Bitcoin DeFi’s demand problem is becoming harder to ignoreBitcoin holders appear unwilling to support dedicated Bitcoin-native DeFi at the scale needed to keep projects in the space alive.

That is the tension behind Botanix Labs' decision to wind down Botanix, a Bitcoin Layer 2 built to bring EVM-style applications, lending, borrowing and yield to BTC holders.

The wind-down is harder to dismiss than a routine token-cycle collapse. Botanix says it deliberately avoided a token, airdrops, points programs and the usual machinery used to manufacture early chain activity.

Demand still fell short.

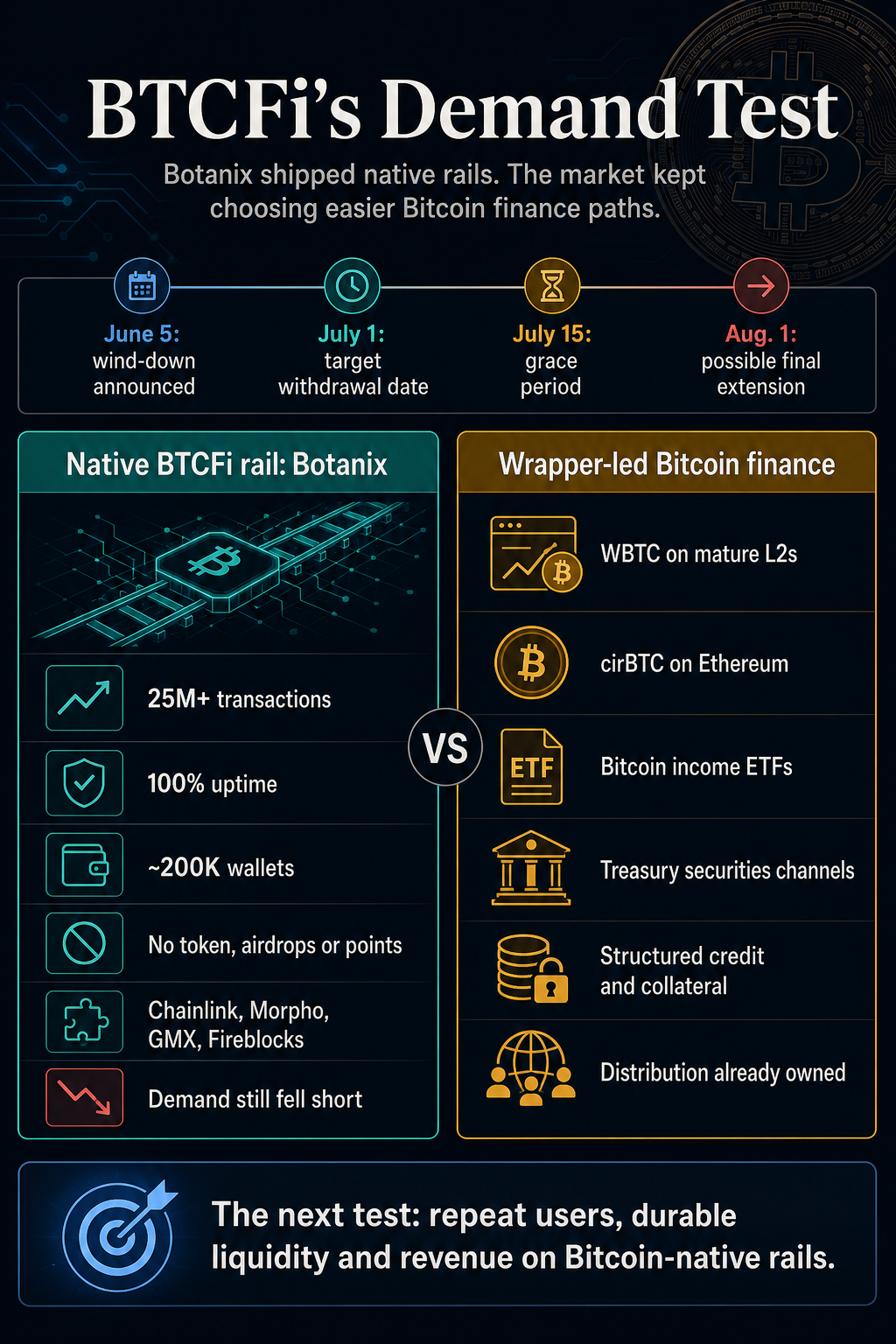

Botanix said its first target wind-down date is July 1, followed by a two-week grace period through July 15 and, if needed, a final extension to Aug. 1 before the remaining Bitcoin is swept and the company begins to dissolve.

Its homepage notice tells users to withdraw assets before the July 1 deadline.

The shutdown lands at an awkward moment for BTCFi. Bitcoin yield, collateral, structured credit and treasury products are becoming more visible across mainstream finance.

Yet one of the cleaner attempts to build Bitcoin-native DeFi rails is leaving the market after concluding that demand was too weak on its own.

What Botanix actually proved

Botanix did not leave behind an empty testnet or a white paper. The team says Spiderchain went live and stayed live for more than a year with 100% uptime and zero security incidents.

It says the network processed 25 million transactions, reached about 200,000 wallets, moved tens of millions of dollars in assets, and secured integrations with Chainlink, Morpho, GMX, Dolomite, Fireblocks, Alchemy, Galaxy, and OKX Wallet.

The current homepage shows the same shape in live-facing terms: more than 26.1 million total transactions, 176,056 unique addresses and 8,387 total contracts.

Those numbers make the failure harder to dismiss. Botanix was building on shipped infrastructure, live usage, and recognized partners, rather than asking the market to imagine a future Bitcoin DeFi layer.

It says it operated one and gave users an organic path into Bitcoin-backed applications without adding a new token as the main economic primitive.

That is why the postmortem is more useful than a normal shutdown notice. It asks whether a working Bitcoin DeFi layer can attract enough users when the product competes with a much easier path: keep BTC where it already is, or use a representation of it elsewhere.

Botanix's own answer is blunt. The team said it mistimed the Bitcoin community's center of gravity.

In its view, Bitcoin holders are still working through questions about BTC as a reserve asset, its political and monetary role, and the conservative culture around the base layer. Programmable utility sits downstream of those concerns.

Some Bitcoin holders clearly want yield, leverage, or access to collateral. Botanix's conclusion is that a dedicated Bitcoin Layer 2 must overcome more than just technical risks.

It has to persuade users that the extra security story, wallet flow, and application set are worth the switch in behavior.

Botanix removed the easy excuse that demand disappeared only after rewards ended.

Its own record raises a harder distribution question: when users can already access BTC products elsewhere, how much extra value does a native rail need to deliver?

The market chose easier rails

The clearest line in Botanix's post is about WBTC. For lending, basic yield and leveraged exposure, the team said WBTC on a mature Layer 2 such as Arbitrum is sufficient for most users who want Bitcoin-denominated DeFi.

That statement cuts through a lot of BTCFi marketing. The practical test is whether enough users care about native Bitcoin rails when they can already borrow, lend or trade against wrapped Bitcoin on venues with deeper liquidity, familiar interfaces and more established applications.

Recent market context points in the same direction. Circle's launch of cirBTC on Ethereum shows the wrapped-BTC fight moving toward custody, reserve visibility, redemption controls and institutional trust.

CryptoSlate's coverage framed the same launch as an attempt to make wrapped Bitcoin look bank-grade before institutions use it as collateral.

That is wrapped Bitcoin finance: BTC exposure converted into a form that risk desks, market makers, lending venues and settlement systems can route through existing workflows.

The same pattern is visible outside DeFi. BlackRock's iShares Bitcoin Premium Income ETF seeks Bitcoin performance while generating premium income through an options strategy.

CryptoSlate reported that Bitcoin is being packaged for income investors through products such as BITA, Metaplanet's Siiibo acquisition, and other yield structures that generate income from options, credit, or collateralized exposure rather than from Bitcoin's protocol.

Metaplanet's Siiibo deal adds another version of the same idea. The Japanese Bitcoin treasury company is trying to turn a BTC balance sheet into a regulated securities channel for bonds, funds and yield-style products.

Terms, approvals, collateral rules, and investor protections remain undisclosed, so the risk profile remains unresolved. The direction is clearer than the product design: Bitcoin is being turned into something brokerages and income investors can buy.

These products also translate Bitcoin into familiar paperwork, accounts and risk frameworks. That translation reduces the behavioral change required from the buyer.

The user may be seeking income, liquidity, or access to collateral, rather than making a statement about Bitcoin's technical roadmap.

Native rails face a distribution problem

Botanix also pointed to a second force: distribution. It named Hyperliquid, Robinhood, major centralized exchanges, and emerging TradFi participants as venues that are absorbing more attention, flow, and revenue because they own the user relationship.

That diagnosis fits the broader Bitcoin finance buildout. CryptoSlate's structured-credit reporting showed that Bitcoin is already being used in insurance reserves, loans, and securitizations, including Ledn's $188 million Bitcoin-backed loan securitization in February 2026, with $160 million of senior notes rated BBB- and $28 million of junior notes rated B-.

CryptoSlate also reported on Morgan Stanley and Galaxy's work around Bitcoin and Ethereum collateral, describing a market where institutions are competing to control the wrapper, custodian, collateral agent or servicing infrastructure through which crypto assets flow.

For a user, those paths often feel less ideologically pure but more legible. A brokerage account, ETF, lending desk or wrapped asset has a known interface.

It may also have clearer disclosures, deeper liquidity, tax reporting, customer support or institutional approval.

A Bitcoin-native DeFi rail must offer sufficient additional value to overcome that convenience gap.

Question

Bitcoin-native BTCFi rails

Wrapper-led Bitcoin finance

Custody story

Attempts to keep the product closer to Bitcoin-native assumptions

Uses custodians, ETFs, wrapped tokens or brokerage platforms

User path

Requires new wallets, bridges, apps and risk decisions

Runs through venues and accounts users already know

Yield source

Needs real application revenue or protocol-level demand

Often comes from options premiums, credit structures or collateral use

Distribution

Must build its own audience

Leans on exchanges, asset managers, banks and brokers

Main risk

Insufficient repeat usage to sustain the network

Complexity, counterparty risk, capped upside or forced-selling loops

That split helps explain why Botanix could be technically credible and commercially exposed at the same time. The network had activity, integrations, and uptime, but the competing channels offered an easier customer path.

The Bitcoin finance boom is splitting into two tracks: productive BTC through wrappers and native BTCFi, which is still fighting for habitual users.

The real BTCFi test

Botanix's shutdown shows that technical credibility and organic metrics are still insufficient if the product fails to align with where users are willing to take risks.

The more precise reading is that Bitcoin DeFi remains caught between two markets. One market wants Bitcoin to stay simple: reserve asset, collateral, treasury holding, long-term store of value.

The other wants Bitcoin to become productive: borrowed against, wrapped, routed into income products, posted as collateral and used inside trading systems.

Botanix tried to connect those markets through Bitcoin-native infrastructure. The growth elsewhere suggests many users and institutions are choosing the second market, but through wrappers that hide the complexity or hand it to a regulated intermediary.

That makes the next BTCFi cycle easier to judge. The test is whether a Bitcoin-native network can produce repeat users, durable liquidity, and sufficient revenue without leaning on a token campaign or relying on users to care about native rails more than convenience.

If the next wave of Bitcoin finance happens on Bitcoin-native infrastructure, Botanix will look early. If it keeps moving through ETFs, wrapped BTC, lending desks, treasury products, and exchange-owned applications, Botanix will look like an honest experiment that discovered where demand actually lives.

The post appeared first on CryptoSlate.

read the full story

Bitcoin holders appear unwilling to support dedicated Bitcoin-native DeFi at the scale needed to keep projects in the space alive.

That is the tension behind Botanix Labs' decision to wind down Botanix, a Bitcoin Layer 2 built to bring EVM-style applications, lending, borrowing and yield to BTC holders.

The wind-down is harder to dismiss than a routine token-cycle collapse. Botanix says it deliberately avoided a token, airdrops, points programs and the usual machinery used to manufacture early chain activity.

Demand still fell short.

Botanix said its first target wind-down date is July 1, followed by a two-week grace period through July 15 and, if needed, a final extension to Aug. 1 before the remaining Bitcoin is swept and the company begins to dissolve.

Its homepage notice tells users to withdraw assets before the July 1 deadline.

The shutdown lands at an awkward moment for BTCFi. Bitcoin yield, collateral, structured credit and treasury products are becoming more visible across mainstream finance.

Yet one of the cleaner attempts to build Bitcoin-native DeFi rails is leaving the market after concluding that demand was too weak on its own.

What Botanix actually proved

Botanix did not leave behind an empty testnet or a white paper. The team says Spiderchain went live and stayed live for more than a year with 100% uptime and zero security incidents.

It says the network processed 25 million transactions, reached about 200,000 wallets, moved tens of millions of dollars in assets, and secured integrations with Chainlink, Morpho, GMX, Dolomite, Fireblocks, Alchemy, Galaxy, and OKX Wallet.

The current homepage shows the same shape in live-facing terms: more than 26.1 million total transactions, 176,056 unique addresses and 8,387 total contracts.

Those numbers make the failure harder to dismiss. Botanix was building on shipped infrastructure, live usage, and recognized partners, rather than asking the market to imagine a future Bitcoin DeFi layer.

It says it operated one and gave users an organic path into Bitcoin-backed applications without adding a new token as the main economic primitive.

That is why the postmortem is more useful than a normal shutdown notice. It asks whether a working Bitcoin DeFi layer can attract enough users when the product competes with a much easier path: keep BTC where it already is, or use a representation of it elsewhere.

Botanix's own answer is blunt. The team said it mistimed the Bitcoin community's center of gravity.

In its view, Bitcoin holders are still working through questions about BTC as a reserve asset, its political and monetary role, and the conservative culture around the base layer. Programmable utility sits downstream of those concerns.

Some Bitcoin holders clearly want yield, leverage, or access to collateral. Botanix's conclusion is that a dedicated Bitcoin Layer 2 must overcome more than just technical risks.

It has to persuade users that the extra security story, wallet flow, and application set are worth the switch in behavior.

Botanix removed the easy excuse that demand disappeared only after rewards ended.

Its own record raises a harder distribution question: when users can already access BTC products elsewhere, how much extra value does a native rail need to deliver?

The market chose easier rails

The clearest line in Botanix's post is about WBTC. For lending, basic yield and leveraged exposure, the team said WBTC on a mature Layer 2 such as Arbitrum is sufficient for most users who want Bitcoin-denominated DeFi.

That statement cuts through a lot of BTCFi marketing. The practical test is whether enough users care about native Bitcoin rails when they can already borrow, lend or trade against wrapped Bitcoin on venues with deeper liquidity, familiar interfaces and more established applications.

Recent market context points in the same direction. Circle's launch of cirBTC on Ethereum shows the wrapped-BTC fight moving toward custody, reserve visibility, redemption controls and institutional trust.

CryptoSlate's coverage framed the same launch as an attempt to make wrapped Bitcoin look bank-grade before institutions use it as collateral.

That is wrapped Bitcoin finance: BTC exposure converted into a form that risk desks, market makers, lending venues and settlement systems can route through existing workflows.

The same pattern is visible outside DeFi. BlackRock's iShares Bitcoin Premium Income ETF seeks Bitcoin performance while generating premium income through an options strategy.

CryptoSlate reported that Bitcoin is being packaged for income investors through products such as BITA, Metaplanet's Siiibo acquisition, and other yield structures that generate income from options, credit, or collateralized exposure rather than from Bitcoin's protocol.

Metaplanet's Siiibo deal adds another version of the same idea. The Japanese Bitcoin treasury company is trying to turn a BTC balance sheet into a regulated securities channel for bonds, funds and yield-style products.

Terms, approvals, collateral rules, and investor protections remain undisclosed, so the risk profile remains unresolved. The direction is clearer than the product design: Bitcoin is being turned into something brokerages and income investors can buy.

These products also translate Bitcoin into familiar paperwork, accounts and risk frameworks. That translation reduces the behavioral change required from the buyer.

The user may be seeking income, liquidity, or access to collateral, rather than making a statement about Bitcoin's technical roadmap.

Native rails face a distribution problem

Botanix also pointed to a second force: distribution. It named Hyperliquid, Robinhood, major centralized exchanges, and emerging TradFi participants as venues that are absorbing more attention, flow, and revenue because they own the user relationship.

That diagnosis fits the broader Bitcoin finance buildout. CryptoSlate's structured-credit reporting showed that Bitcoin is already being used in insurance reserves, loans, and securitizations, including Ledn's $188 million Bitcoin-backed loan securitization in February 2026, with $160 million of senior notes rated BBB- and $28 million of junior notes rated B-.

CryptoSlate also reported on Morgan Stanley and Galaxy's work around Bitcoin and Ethereum collateral, describing a market where institutions are competing to control the wrapper, custodian, collateral agent or servicing infrastructure through which crypto assets flow.

For a user, those paths often feel less ideologically pure but more legible. A brokerage account, ETF, lending desk or wrapped asset has a known interface.

It may also have clearer disclosures, deeper liquidity, tax reporting, customer support or institutional approval.

A Bitcoin-native DeFi rail must offer sufficient additional value to overcome that convenience gap.

| Question | Bitcoin-native BTCFi rails | Wrapper-led Bitcoin finance |

|---|---|---|

| Custody story | Attempts to keep the product closer to Bitcoin-native assumptions | Uses custodians, ETFs, wrapped tokens or brokerage platforms |

| User path | Requires new wallets, bridges, apps and risk decisions | Runs through venues and accounts users already know |

| Yield source | Needs real application revenue or protocol-level demand | Often comes from options premiums, credit structures or collateral use |

| Distribution | Must build its own audience | Leans on exchanges, asset managers, banks and brokers |

| Main risk | Insufficient repeat usage to sustain the network | Complexity, counterparty risk, capped upside or forced-selling loops |

That split helps explain why Botanix could be technically credible and commercially exposed at the same time. The network had activity, integrations, and uptime, but the competing channels offered an easier customer path.

The Bitcoin finance boom is splitting into two tracks: productive BTC through wrappers and native BTCFi, which is still fighting for habitual users.

The real BTCFi test

Botanix's shutdown shows that technical credibility and organic metrics are still insufficient if the product fails to align with where users are willing to take risks.

The more precise reading is that Bitcoin DeFi remains caught between two markets. One market wants Bitcoin to stay simple: reserve asset, collateral, treasury holding, long-term store of value.

The other wants Bitcoin to become productive: borrowed against, wrapped, routed into income products, posted as collateral and used inside trading systems.

Botanix tried to connect those markets through Bitcoin-native infrastructure. The growth elsewhere suggests many users and institutions are choosing the second market, but through wrappers that hide the complexity or hand it to a regulated intermediary.

That makes the next BTCFi cycle easier to judge. The test is whether a Bitcoin-native network can produce repeat users, durable liquidity, and sufficient revenue without leaning on a token campaign or relying on users to care about native rails more than convenience.

If the next wave of Bitcoin finance happens on Bitcoin-native infrastructure, Botanix will look early. If it keeps moving through ETFs, wrapped BTC, lending desks, treasury products, and exchange-owned applications, Botanix will look like an honest experiment that discovered where demand actually lives.

The post appeared first on CryptoSlate.

read the full storyCME Group to Sue CFTC Over Approval of Bitcoin Perpetual Futures

The dispute centers on whether perpetual contracts should be regulated as futures or swaps under…

Tether Trims Bitdeer Stake After AI Push Lifts Bitcoin Mining Stock

Tether has started trimming its Bitdeer (NASDAQ: BTDR) stake after reloading on the bitcoin mining…

Binance users boost BTC, ETH holdings in latest PoR report

Binance’s 43rd proof of reserves shows user BTC and ETH balances rising in June, while USDT…

Fed Surprises Markets, Gold Drops $40 and Bitcoin Slips Under $65,500

Gold got hit hard Wednesday. Prices fell more than $40 per ounce in a single session, and Bitcoin…

The bond market is flashing a clear signal on interest rates. Bitcoin bulls should take note

The bond market is sending a signal that complicates prospects of a near-term bitcoin bull run.

Yield Basis Deposits Jump 120% in 2 Weeks as Investors Seek BTC Yield Without Selling

Yield Basis says deposits into its new Hybrid Vaults rose more than 120% in under two weeks,…

Trump Signs the US-Iran Peace MoU, but the Fed Stops Bitcoin’s Recovery Cold

Donald Trump signed the US-Iran peace Memorandum of Understanding (MoU), marking a historic…

Bitcoin Whale Wallets See Major Rebound

Bitcoin's largest holders are staging a massive accumulation campaign, reversing months of selling…

Live markets: Bitcoin and ether ETFs lost $111 million combined as rate-cut hopes died

Total market value has held flat near $2.26 trillion since Tuesday, with the recovery losing…

Buying bitcoin below its 200-week average has historically delivered over 100% in median returns, Kraken says

Bitcoin briefly slipped below its 200-week moving average twice in the past two weeks, a rare event…

Michael Saylor Calls Bitcoin the Base Layer for a New Digital Capital Stack

The Strategy chair believes Bitcoin can jump 500-fold, but this depends more on large-scale…

HyperFund Promoter ‘Bitcoin Rodney’ Pleads Guilty in $1.8 Billion Crypto Scam

HyperFund drew $1.8 billion from investors worldwide through a crypto platform prosecutors described…

Bitcoin, ether slide after a hawkish Fed, even as Trump's signed Iran deal lifts stocks

The Fed held rates but signaled it is more worried about inflation than growth in Chair Kevin…

Tether winds down gold-backed derivative stablecoin aUSDT

Tether is focusing on stronger user demand, deeper liquidity, and broader long-term market…

Oman Launches Mandatory National Bitcoin Mining Pool In Sovereign Regulatory Push

Omanhash.om is being positioned as the official mining pool for licensed crypto miners in Oman,…

Bitcoin Eyes $70K Breakout as 21Shares Sees Path Toward $100K by Q3

Bitcoin remains above a key support zone despite a Federal Reserve-driven pullback, while 21Shares…

France to Phase Out Non-Quantum Encryption as Bitcoin Security Concerns Grow

French authorities said that government cybersecurity researchers will stop certifying security…

Hyperliquid (HYPE), Bitcoin (BTC), XRP and Dogecoin (DOGE) Price Analysis for June 17: Reclaiming the Bullish Narrative

Crypto markets are showing mixed recovery signals, with some assets holding strong uptrends while…

Illinois Targets Bitcoin Transactions With New Tax Critics Call ‘Punitive’

TL;DR: Levy amount: The legislation permanently establishes a 0.2% rate on the transfer or purchase…