A US Bitcoin treasury company sold every BTC because debt and Nasdaq pressure just closed inK Wave Media has become a new case study for corporate Bitcoin trade stress.

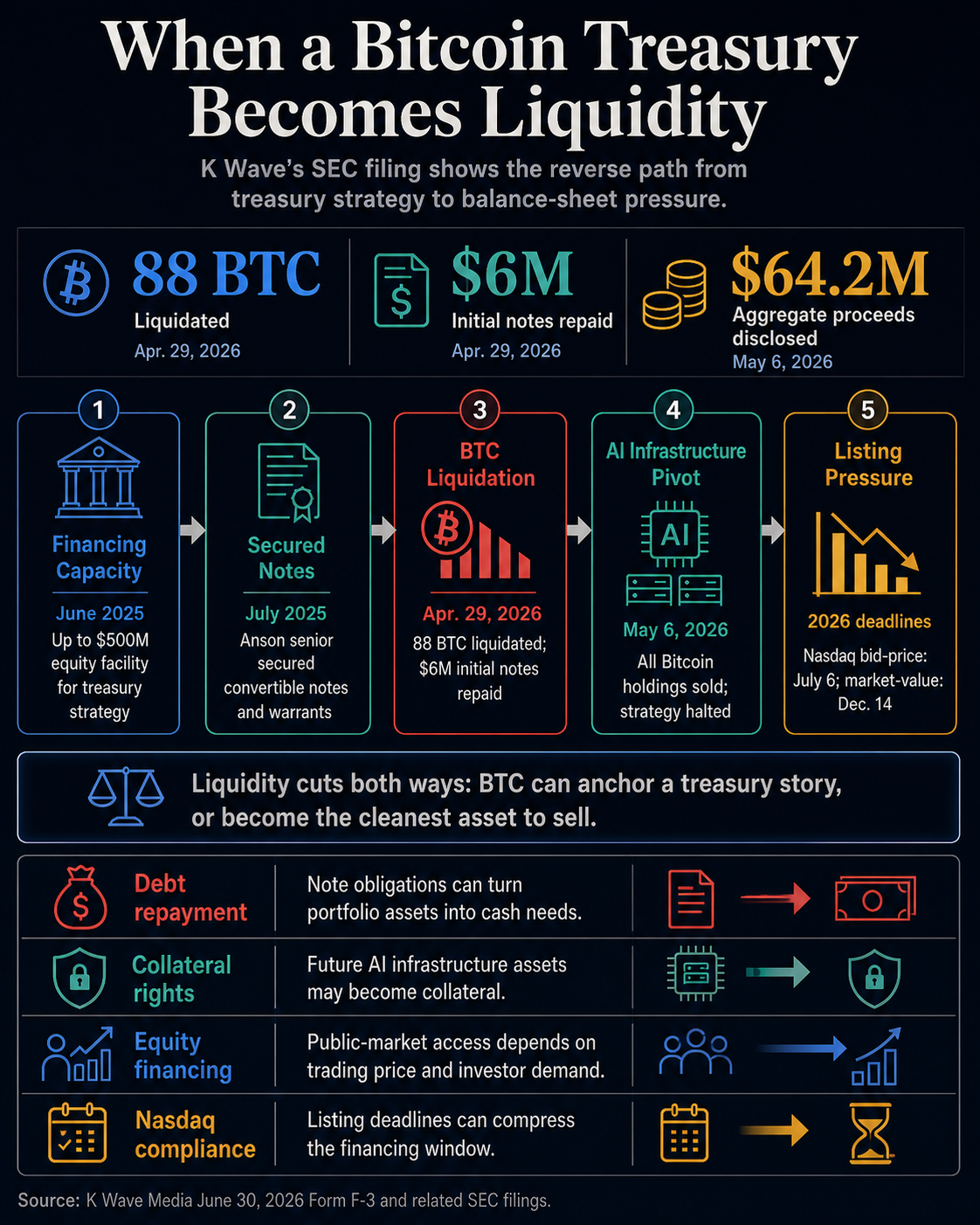

In a June 30 Form F-3, the Nasdaq-listed company disclosed that it sold all of its Bitcoin holdings on May 6 and said the sale generated aggregate proceeds of $64.2 million.

The filing also said K Wave had liquidated 88 Bitcoins under an April 29 amendment to its securities purchase agreement with Anson Funds and used part of the transaction to repay $6 million of initial notes.

The filing frames the sale through financing, collateral and strategic-priority disclosures rather than an explicit forced-sale statement. Its value lies in the mechanics it exposes: a Bitcoin balance sheet can shift from a permanent reserve narrative to a liquid asset when financing priorities change.

K Wave said the treasury strategy was halted while it focused on AI infrastructure, even as the company said it had not entirely abandoned the plan. That distinction puts the company’s financing documents, collateral language and Nasdaq compliance problems in the foreground.

For investors who have rewarded public companies for announcing Bitcoin purchases, K Wave is the reverse case. The filing points to a fragile version of the treasury trade, where the key question is whether a company’s capital structure allows it to keep holding when debt, collateral, and listing rules become more stringent.

The filing moves Bitcoin from treasury story to balance-sheet story

K Wave's Bitcoin plan started with financing capacity. A June 2025 filing described a standby equity purchase agreement with Bitcoin Strategic Reserve KWM LLC that gave the company the right to sell up to $500 million of ordinary shares, subject to conditions.

Later registration materials stated that proceeds from sales to Bitcoin Strategic were expected to be used primarily for working capital, general corporate purposes, and the implementation of the company's treasury strategy.

The June 30 F-3 shows how far that structure had moved by 2026. K Wave disclosed that it had entered into a securities purchase agreement with Anson Funds in July 2025, under which the company agreed to issue senior secured convertible notes and warrants.

The initial closing generated $15 million in gross proceeds through notes and warrants. The structure also contemplated potential additional notes and warrants, subject to conditions.

The April 29 amendment is the turning point. According to the F-3, K Wave liquidated 88 Bitcoin held in its treasury and repaid $6 million of the initial notes.

The same amendment allowed proceeds from future sales of additional securities under the Anson agreement to be used for AI infrastructure assets. Those AI infrastructure assets would then become collateral under the company's security agreement.

The market-structure point is straightforward: the Bitcoin treasury sat on a public company's balance sheet that also included convertible debt, warrants, futures securities sales, collateral rights, and a new business plan built around AI infrastructure.

The company also said in the filing that it sold all of its Bitcoin holdings on May 6. The filing presents the $64.2 million proceeds figure separately from the 88 BTC liquidation disclosure, so the number is best read as the company's stated aggregate proceeds rather than independent price math.

The direction of travel is the main point for the treasury trade. K Wave disclosed a full exit from Bitcoin while shifting financing capacity toward another capital-intensive strategy.

Debt and collateral change the meaning of a Bitcoin reserve

Bitcoin treasury companies often present BTC as a strategic reserve. K Wave's filing shows how quickly that phrase can become more complicated once the reserve is attached to debt documents.

The Anson notes carried ordinary-share conversion rights and alternate conversion mechanics tied to trading prices. The filing also said the notes would bear no interest unless an event of default occurred, in which case they would bear interest at 12% annually, retroactive from issuance.

The same document described default provisions under which outstanding principal, accrued interest and other amounts could be accelerated.

The collateral language is especially important. The F-3 said that if K Wave defaults on its secured obligations, the secured party would have the right to take exclusive control of the collateral and sell, dispose of, or transfer it until the secured obligations are paid in full.

If those remedies were insufficient, K Wave would remain liable for the deficiency.

The filing gives no basis to attribute the Bitcoin sale to a default, and it shows why the word “reserve” can be misleading for smaller treasury companies that finance their strategies through convertible notes, warrants, equity facilities, and secured obligations.

A reserve can be strategic in one respect and economically available in another.

K Wave's shift toward AI infrastructure sharpened that point. A May 4 exhibit said the company was redirecting remaining financing capacity toward AI infrastructure and connected the shift to liability reduction.

The F-3 then tied future AI infrastructure assets to collateral under the security agreement.

That creates a substantial collision. Bitcoin competed with debt repayment, collateral packages and a corporate attempt to reposition around data centers, GPU infrastructure and AI compute.

Together, those disclosures turn the Bitcoin sale into part of a broader capital-allocation sequence: repay notes, reshape collateral, preserve financing options and move toward a new infrastructure thesis.

Nasdaq pressure made the financing window matter

K Wave's public-market position added another layer of pressure.

The F-3 said Nasdaq notified the company in January that it no longer met the exchange's $1 minimum bid-price requirement after its closing bid price stayed below the threshold from Nov. 20, 2025, to Jan. 6, 2026.

K Wave had until July 6, 2026, to regain compliance. The company said it was evaluating options, including a reverse stock split subject to shareholder approval.

A second deficiency followed in June. Nasdaq told K Wave that its ordinary shares did not meet the $15 million minimum market value of publicly held shares requirement for the period from May 4 to June 15.

The company had until Dec. 14, 2026, to regain compliance, according to the F-3 and a June 18 filing exhibit.

The June 30 registration statement also said K Wave's ordinary shares closed at $0.164 on June 29. That share price is more than market color. For a company whose treasury strategy relied on public-market financing tools, trading price, listing status and investor appetite shape what financing is actually usable.

This is where smaller treasury companies differ from the largest names in the trade. Large holders with deep liquidity and repeated access to capital markets may be able to continue adding Bitcoin during volatile periods.

Smaller issuers can face a different equation. A falling stock price can weaken equity issuance, make conversion terms more important, make collateral central, and force corporate actions while management tries to defend a strategic narrative.

K Wave's filing indicates that the trade can be reversed through normal public-company channels. Debt gets amended. Collateral packages change. New uses of proceeds appear. Listing deadlines approach. A treasury reserve becomes part of a broader capital-allocation problem.

That progression is the live signal for the rest of the cohort. When financing documents, listing notices, and collateral packages start moving at the same time, investors have to judge whether Bitcoin remains protected treasury property or becomes the most liquid asset on the balance sheet.

The broader Bitcoin treasury trade is moving from accumulation to durability

K-Wave's exit comes as investors are already rethinking how they evaluate corporate Bitcoin strategies.

CryptoSlate has tracked the shift from headline BTC accumulation to questions about financing, dilution, debt, and whether companies can hold through stress. In May, CryptoSlate noted that the Bitcoin treasury trade was facing a stress test as some corporate holders used BTC to raise cash, repay debt or fund operations.

More recently, CryptoSlate reported that investors were turning on treasury companies that relied on dilution to keep buying.

Bitcoin remains the reference asset for the whole trade. CryptoSlate's July 2 Bitcoin market data showed BTC near $60,000, with a market cap around $1.21 trillion and dominance of about 58% across the crypto market. So, the asset remains large and liquid enough to anchor corporate treasury narratives. That liquidity is also why it can become the asset sold when another obligation takes priority.

The next test extends beyond whether companies announce more BTC purchases. It is whether the filings show that those purchases are durable after accounting for financing costs, preferred dividends, note terms, collateral rights, share-price weakness, and listing compliance.

For stronger treasury companies, a stabilized financing window could preserve the option to hold or keep accumulating. For weaker companies, the same market can look different. Bitcoin may be the cleanest asset to sell, the easiest source of cash, or the clearest way to satisfy a changed financing agreement.

K Wave is now the filing-level example of that second path.

The company's disclosure leaves the broader treasury trade intact, but it makes the downside mechanics harder to ignore. A Bitcoin treasury strategy is only as permanent as the balance sheet beneath it, and K Wave's June 30 filing shows what happens when the balance sheet starts pointing somewhere else.

The post appeared first on CryptoSlate.

read the full story

K Wave Media has become a new case study for corporate Bitcoin trade stress.

In a June 30 Form F-3, the Nasdaq-listed company disclosed that it sold all of its Bitcoin holdings on May 6 and said the sale generated aggregate proceeds of $64.2 million.

The filing also said K Wave had liquidated 88 Bitcoins under an April 29 amendment to its securities purchase agreement with Anson Funds and used part of the transaction to repay $6 million of initial notes.

The filing frames the sale through financing, collateral and strategic-priority disclosures rather than an explicit forced-sale statement. Its value lies in the mechanics it exposes: a Bitcoin balance sheet can shift from a permanent reserve narrative to a liquid asset when financing priorities change.

K Wave said the treasury strategy was halted while it focused on AI infrastructure, even as the company said it had not entirely abandoned the plan. That distinction puts the company’s financing documents, collateral language and Nasdaq compliance problems in the foreground.

For investors who have rewarded public companies for announcing Bitcoin purchases, K Wave is the reverse case. The filing points to a fragile version of the treasury trade, where the key question is whether a company’s capital structure allows it to keep holding when debt, collateral, and listing rules become more stringent.

The filing moves Bitcoin from treasury story to balance-sheet story

K Wave's Bitcoin plan started with financing capacity. A June 2025 filing described a standby equity purchase agreement with Bitcoin Strategic Reserve KWM LLC that gave the company the right to sell up to $500 million of ordinary shares, subject to conditions.

Later registration materials stated that proceeds from sales to Bitcoin Strategic were expected to be used primarily for working capital, general corporate purposes, and the implementation of the company's treasury strategy.

The June 30 F-3 shows how far that structure had moved by 2026. K Wave disclosed that it had entered into a securities purchase agreement with Anson Funds in July 2025, under which the company agreed to issue senior secured convertible notes and warrants.

The initial closing generated $15 million in gross proceeds through notes and warrants. The structure also contemplated potential additional notes and warrants, subject to conditions.

The April 29 amendment is the turning point. According to the F-3, K Wave liquidated 88 Bitcoin held in its treasury and repaid $6 million of the initial notes.

The same amendment allowed proceeds from future sales of additional securities under the Anson agreement to be used for AI infrastructure assets. Those AI infrastructure assets would then become collateral under the company's security agreement.

The market-structure point is straightforward: the Bitcoin treasury sat on a public company's balance sheet that also included convertible debt, warrants, futures securities sales, collateral rights, and a new business plan built around AI infrastructure.

The company also said in the filing that it sold all of its Bitcoin holdings on May 6. The filing presents the $64.2 million proceeds figure separately from the 88 BTC liquidation disclosure, so the number is best read as the company's stated aggregate proceeds rather than independent price math.

The direction of travel is the main point for the treasury trade. K Wave disclosed a full exit from Bitcoin while shifting financing capacity toward another capital-intensive strategy.

Debt and collateral change the meaning of a Bitcoin reserve

Bitcoin treasury companies often present BTC as a strategic reserve. K Wave's filing shows how quickly that phrase can become more complicated once the reserve is attached to debt documents.

The Anson notes carried ordinary-share conversion rights and alternate conversion mechanics tied to trading prices. The filing also said the notes would bear no interest unless an event of default occurred, in which case they would bear interest at 12% annually, retroactive from issuance.

The same document described default provisions under which outstanding principal, accrued interest and other amounts could be accelerated.

The collateral language is especially important. The F-3 said that if K Wave defaults on its secured obligations, the secured party would have the right to take exclusive control of the collateral and sell, dispose of, or transfer it until the secured obligations are paid in full.

If those remedies were insufficient, K Wave would remain liable for the deficiency.

The filing gives no basis to attribute the Bitcoin sale to a default, and it shows why the word “reserve” can be misleading for smaller treasury companies that finance their strategies through convertible notes, warrants, equity facilities, and secured obligations.

A reserve can be strategic in one respect and economically available in another.

K Wave's shift toward AI infrastructure sharpened that point. A May 4 exhibit said the company was redirecting remaining financing capacity toward AI infrastructure and connected the shift to liability reduction.

The F-3 then tied future AI infrastructure assets to collateral under the security agreement.

That creates a substantial collision. Bitcoin competed with debt repayment, collateral packages and a corporate attempt to reposition around data centers, GPU infrastructure and AI compute.

Together, those disclosures turn the Bitcoin sale into part of a broader capital-allocation sequence: repay notes, reshape collateral, preserve financing options and move toward a new infrastructure thesis.

Nasdaq pressure made the financing window matter

K Wave's public-market position added another layer of pressure.

The F-3 said Nasdaq notified the company in January that it no longer met the exchange's $1 minimum bid-price requirement after its closing bid price stayed below the threshold from Nov. 20, 2025, to Jan. 6, 2026.

K Wave had until July 6, 2026, to regain compliance. The company said it was evaluating options, including a reverse stock split subject to shareholder approval.

A second deficiency followed in June. Nasdaq told K Wave that its ordinary shares did not meet the $15 million minimum market value of publicly held shares requirement for the period from May 4 to June 15.

The company had until Dec. 14, 2026, to regain compliance, according to the F-3 and a June 18 filing exhibit.

The June 30 registration statement also said K Wave's ordinary shares closed at $0.164 on June 29. That share price is more than market color. For a company whose treasury strategy relied on public-market financing tools, trading price, listing status and investor appetite shape what financing is actually usable.

This is where smaller treasury companies differ from the largest names in the trade. Large holders with deep liquidity and repeated access to capital markets may be able to continue adding Bitcoin during volatile periods.

Smaller issuers can face a different equation. A falling stock price can weaken equity issuance, make conversion terms more important, make collateral central, and force corporate actions while management tries to defend a strategic narrative.

K Wave's filing indicates that the trade can be reversed through normal public-company channels. Debt gets amended. Collateral packages change. New uses of proceeds appear. Listing deadlines approach. A treasury reserve becomes part of a broader capital-allocation problem.

That progression is the live signal for the rest of the cohort. When financing documents, listing notices, and collateral packages start moving at the same time, investors have to judge whether Bitcoin remains protected treasury property or becomes the most liquid asset on the balance sheet.

The broader Bitcoin treasury trade is moving from accumulation to durability

K-Wave's exit comes as investors are already rethinking how they evaluate corporate Bitcoin strategies.

CryptoSlate has tracked the shift from headline BTC accumulation to questions about financing, dilution, debt, and whether companies can hold through stress. In May, CryptoSlate noted that the Bitcoin treasury trade was facing a stress test as some corporate holders used BTC to raise cash, repay debt or fund operations.

More recently, CryptoSlate reported that investors were turning on treasury companies that relied on dilution to keep buying.

Bitcoin remains the reference asset for the whole trade. CryptoSlate's July 2 Bitcoin market data showed BTC near $60,000, with a market cap around $1.21 trillion and dominance of about 58% across the crypto market. So, the asset remains large and liquid enough to anchor corporate treasury narratives. That liquidity is also why it can become the asset sold when another obligation takes priority.

The next test extends beyond whether companies announce more BTC purchases. It is whether the filings show that those purchases are durable after accounting for financing costs, preferred dividends, note terms, collateral rights, share-price weakness, and listing compliance.

For stronger treasury companies, a stabilized financing window could preserve the option to hold or keep accumulating. For weaker companies, the same market can look different. Bitcoin may be the cleanest asset to sell, the easiest source of cash, or the clearest way to satisfy a changed financing agreement.

K Wave is now the filing-level example of that second path.

The company's disclosure leaves the broader treasury trade intact, but it makes the downside mechanics harder to ignore. A Bitcoin treasury strategy is only as permanent as the balance sheet beneath it, and K Wave's June 30 filing shows what happens when the balance sheet starts pointing somewhere else.

The post appeared first on CryptoSlate.

read the full storyBitcoin Traders Brace for $62K Test After Rebound From $57,735 Low

Bitcoin climbed to $61,211 early Thursday, a rebound of more than 5% off its 24-hour low. The move…

Is The Bottom Finally Here? BTC, ETH, XRP, and SOL Flash Buy Signals

"Your window to buy crypto this cheap is almost gone," one analyst argued.

Bitcoin is trading like a tech stock, not gold

Bitcoin tech stock correlation rose as BTC fell 50% with the Nasdaq while gold hit records. Is…

Bitcoin miners are selling: is capitulation here?

Public Bitcoin miners sold a record 32,000 BTC as hashprice hit post-halving lows and rigs switch…

Smaller tokens lead as bitcoin, sol rally in 'first real bounce of the selloff'

Bitcoin and major cryptocurrencies rebounded on dovish Federal Reserve signals, with speculative…

Crypto ETFs Split as Ether, HYPE and Solana Gain While Bitcoin Loses $295 Million

Crypto ETF flows remained uneven on Wednesday, July 1, as bitcoin funds posted a $294.62 million…

Bitcoin Reclaims $60K as SOL, BCH Lead Alts Higher (Market Watch)

Bitcoin managed to bounce from yesterday's lows, while the majority of large-cap altcoins also…

SBI Crypto shuts Bitcoin mining pool after 5-year run

SBI Crypto will shut down its Bitcoin mining pool on July 31 after more than five years, ranking…

Bitcoin zooms above $61,000 as inflation fears soften

Bitcoin rose more than 4% to trade above $61,000, its strongest level in over a week, after Fed…

Metaplanet Hits 43,000 BTC Milestone, Now the World’s 3rd Largest Corporate Holder

Metaplanet hit the 43,000 BTC milestone on July 2. The Tokyo-based firm now ranks as the…

3 On-Chain Signals Point to Deepening Bitcoin Capitulation

Bitcoin (BTC) just recorded its worst month since June 2022, falling 20.48% amid contracting demand…

Yield-bearing stablecoin slowdown ends 3-year run for crypto-native products

Yield-bearing stablecoin supply fell 15% in Q2 as sUSDe and sUSDS contracted, while Treasury-backed…

Will Bitcoin price continue uptrend or succumb once again to ETF outflows?

Bitcoin price has rebounded above $60,000 after easing oil prices and softer U.S. macro expectations…

HashKey Capital launches Bitcoin Hashrate Fund with BITMAIN

HashKey Capital will launch a BTC-denominated Bitcoin Hashrate Fund with BITMAIN providing computing…

Metaplanet buys another $170 million of bitcoin expanding treasury to 43,000 BTC

The Japanese firm, now the world's third largest publicly traded bitcoin holder, reported stronger…

Metaplanet buys 2,823 BTC, surpasses 43,000 in Bitcoin holdings

Metaplanet bought 2,823 Bitcoin during the second quarter, reducing its average acquisition cost to…

43,000 Bitcoin Milestone: Japanese Metaplanet Locks Down Global Top 3 Rank

Japan’s Metaplanet enters the global top 3 with 43,000 BTC.