U.S. spot Bitcoin ETFs assets stood at $77.58Bn as of June 10, 2026, precisely where they were the week Donald Trump won the presidential election in November 2024. In the intervening 19 months, these funds climbed to a record $169.54Bn, then bled back every dollar of those gains.

Over just the past four weeks, Bitcoin ETF outflows exceeded $5Bn, accelerating a slide that has erased nearly half of the product category’s peak value.

Here is the central tension this article unpacks: the most crypto-friendly regulatory environment in U.S. history is running in parallel with sustained institutional selling, and understanding why those two things can coexist tells you everything about what Bitcoin ETFs actually are.

Spot Bitcoin ETF AUM: What the $77.6Bn Number Actually Tells You

Think of a spot Bitcoin ETF like a storage facility for institutional money. Investors don’t hold Bitcoin directly; they hold a share of a fund that holds Bitcoin on their behalf. The total value of Bitcoin sitting in all those storage lockers is what we call assets under management, or AUM. When AUM drops, it means either the price of Bitcoin fell, investors pulled their money out, or both.

In this case, it’s both. The 11 U.S. spot Bitcoin ETFs tracked by SoSoValue collectively peaked at $169.54Bn in October 2025, when cumulative net inflows since the January 2024 launch had reached $62.77Bn. As of June 9, 2026, cumulative net inflows have declined by nearly $9Bn to $53.77Bn, the lowest level since August 2025. That means roughly $9Bn in actual investor capital has walked out the door since the peak, on top of price-driven losses.

The funds are not equally affected. BlackRock’s IBIT and Fidelity’s FBTC together control well over half of all spot Bitcoin ETF AUM, and BlackRock’s IBIT had, at one point, accumulated more than $60Bn on its own, overtaking Grayscale’s converted GBTC as the largest single Bitcoin fund on earth. Our earlier breakdown of IBIT as an institutional on-ramp explains why that concentration matters for retail investors reading headline AUM figures.

The uncomfortable truth is that $77.58Bn still represents over 1.26 million BTC held in ETF wrappers, roughly 6% of the circulating supply, locked into products that didn’t exist two years ago. The storage facility isn’t empty. But it is meaningfully less full than it was, and the doors are swinging outward right now.

Rotation, Not Retreat: What’s Actually Driving $5Bn in Bitcoin ETF Outflows

Analysts are not pointing to a crisis of confidence in Bitcoin itself. They’re pointing to a queue of competing priorities draining the same pool of institutional capital.

Binance Research framed the macro picture plainly: “ETF outflows reflected short-term pressure as inflation drives the Fed hawkish, while on-chain supply tightening remains intact.” Translation: sticky inflation is keeping the Federal Reserve in a restrictive posture, and as rates rise, the cost of holding non-yielding assets rises too, prompting institutional allocators to trim exposure to Bitcoin first.

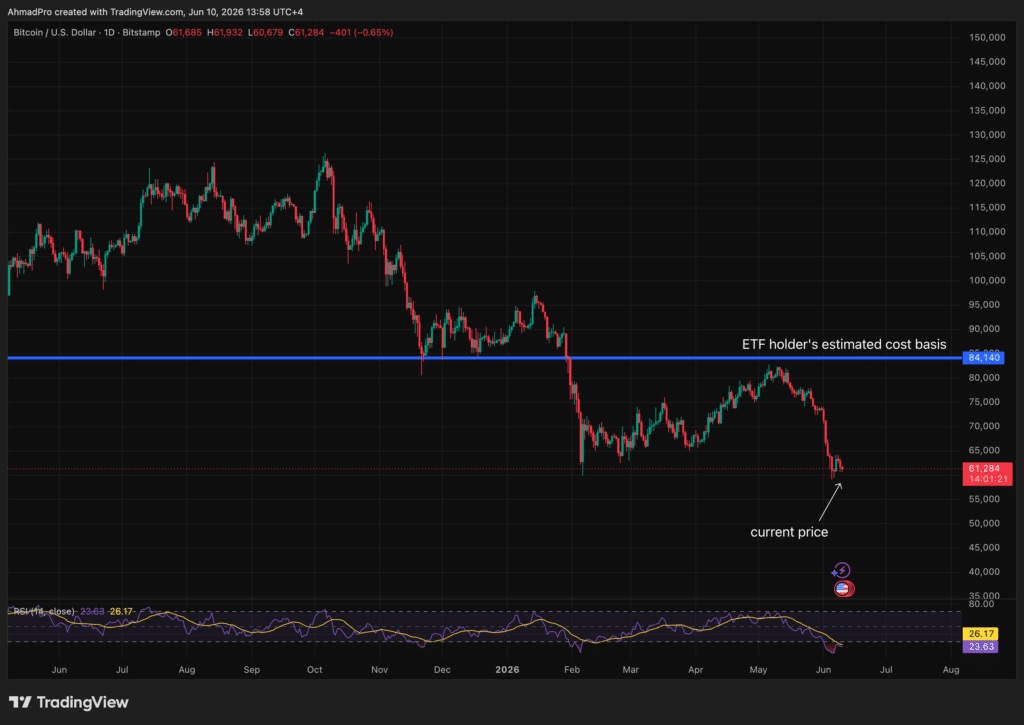

The average ETF holder’s estimated cost basis sits around $84,000, above current spot levels near $61,000, suggesting many are sitting on paper losses and have a reduced appetite to add.

But the macro pressure alone doesn’t explain the full picture. Ophelia Snyder, market analyst and former co-founder of 21Shares, identified the competition dimension clearly: “You have ETF outflows as investors are increasingly distracted by other narratives competing for attention and capital, whether that’s AI, SpaceX, or other high-profile growth stories.

You have ongoing market jitters around geopolitics, the Strait of Hormuz, U.S. jobs data, inflation, and broader macroeconomic uncertainty.” Capital doesn’t disappear; it rotates. And right now, AI infrastructure plays and pre-IPO vehicles are pulling hard.

There’s a third competitor that gets less attention: tokenized treasury products. On-chain U.S. Treasury instruments from issuers like Ondo and Franklin OnChain have climbed into the multi-billion-dollar range, offering yield-bearing, dollar-denominated exposure that sits inside the same “digital asset allocation” bucket many institutions use for Bitcoin ETFs.

For a risk-averse allocator facing a hawkish Fed, a tokenized treasury yielding 5%+ is a real alternative to a Bitcoin ETF sitting in the red.

The on-chain supply picture, which Binance Research specifically flagged as “intact”, argues that long-term holders are not distributing. The Bitcoin ETF news cycle looks worse than the structural reality. This reads as rotation, not retreat.