Bitcoin is approaching a point where the market may have to choose between two very different outcomes. Traders are still paying to stay short, yet price, ETF flows, and market leadership are no longer behaving as if the market were stuck in a collapse.

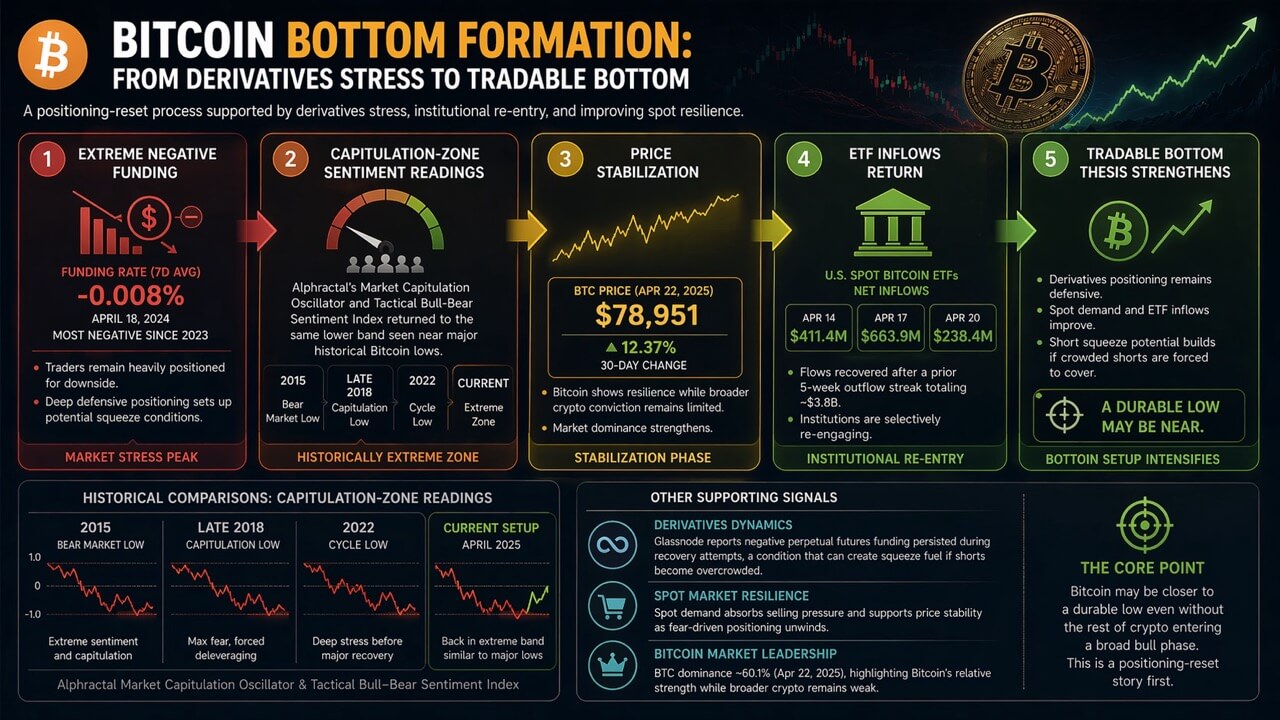

In a recent X post, Alphractal analysts argued that Bitcoin funding rates had reached their most negative level since 2023 and said its proprietary models were pointing to a possible local bottom.

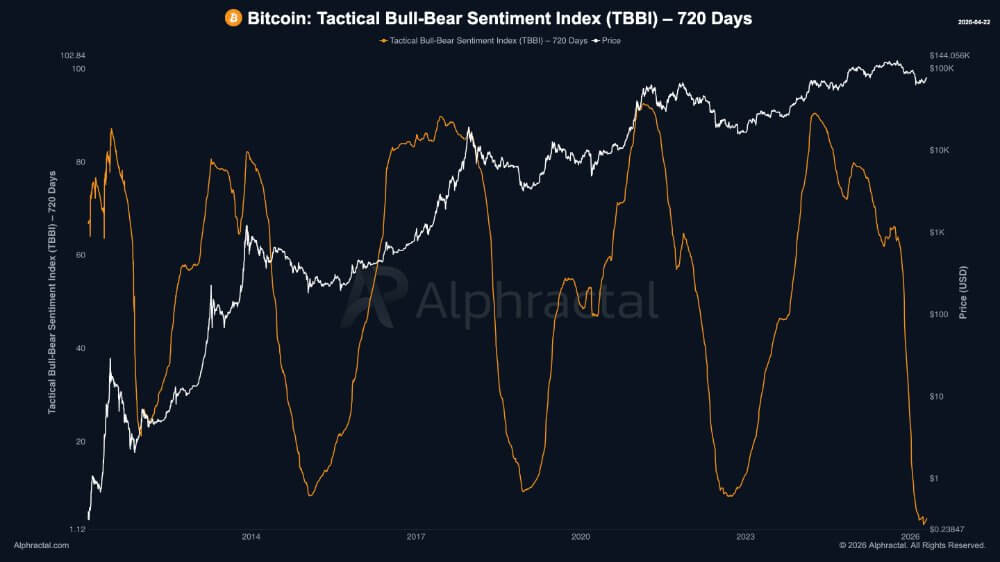

Using its ‘Market Capitulation Oscillator and Tactical Bull-Bear Sentiment Index', they argued that it had dropped into the same extreme zone that had previously appeared near major Bitcoin lows.

In the chart below, the sentiment index falls into deep troughs around earlier cycle washouts, including the 2015 bear-market bottom, the late-2018 capitulation, and the 2022 low.

The latest reading shows the indicator back in that same lower band, which supports the broader argument that market positioning has again reached an unusually stressed level.

Market Capitulation Oscillator and Tactical Bull-Bear Sentiment Index chart (Source: Alphractal)

Thus, Bitcoin seems to be trading in a zone that has previously coincided with capitulation and eventual reversal. Other market data tells a similar story.

Crypto.com said the seven-day average funding rate fell to roughly -0.008% on April 18, the weakest reading since 2023, while Glassnode said negative funding persisted even as Bitcoin stabilized and spot conditions improved.

That leaves the market in an unusual state. Bitcoin may be emerging from a positioning washout that can support a tradable rebound, or the same macro pressures that drove the drawdown may still be strong enough to force one more deeper leg lower.

CryptoSlate'sBitcoin price page shows BTC at $78,951 on April 22, up 12.37% over 30 days, with 60.1% market dominance. The market is not showing the conditions of a broad speculative breakout, but it is showing an asset regaining leadership while conviction elsewhere remains thin.

That distinction is central to the real question. Bitcoin can be closer to a durable low while the rest of crypto remains unready for a full bull-market expansion.

Why the bottoming case has become harder to dismiss

The bullish argument is gaining support from the way spot demand has held up while derivatives positioning remains defensive.

Glassnode described a market where perpetual-futures funding stayed negative even as Bitcoin tried to recover from its drawdown. Sustained negative funding can become fuel for upside when shorts grow crowded, and price starts moving against them, though it also shows that leveraged conviction remains cautious.

The signal gets more interesting because the price has stopped following the same bearish script. Bitcoin is trading less like an asset trapped in one-way liquidation and more like one that has found buyers willing to absorb macro fear.

Those buyers are showing up in one of the cycle's most important channels, the ETF complex. According to Farside Investors, U.S. spot Bitcoin ETFs pulled in $411.4 million on April 14, $663.9 million on April 17, and another $238.4 million on April 20.

That flow pattern shows that larger allocators did not vanish when the market turned tense.

The rebound also looks more credible because it follows a real institutional reset. By the start of March, spot Bitcoin ETFs had already experienced a five-week outflow streak totaling roughly $3.8 billion, before flows began to recover in early March.

That earlier washout helps define the current setup. Institutions appear to have de-risked and are now re-engaging more selectively.

If that process continues while funding stays negative or only gradually normalizes, the short side becomes more vulnerable to a squeeze than the current mood implies. That is the strongest version of the bottoming case, and it does not require declaring that a full-cycle bull market has already begun.

Why macro and policy still cap the upside

The market will now decide whether a tactical rebound can turn into something broader and more durable. That is where the constraints become harder to ignore.

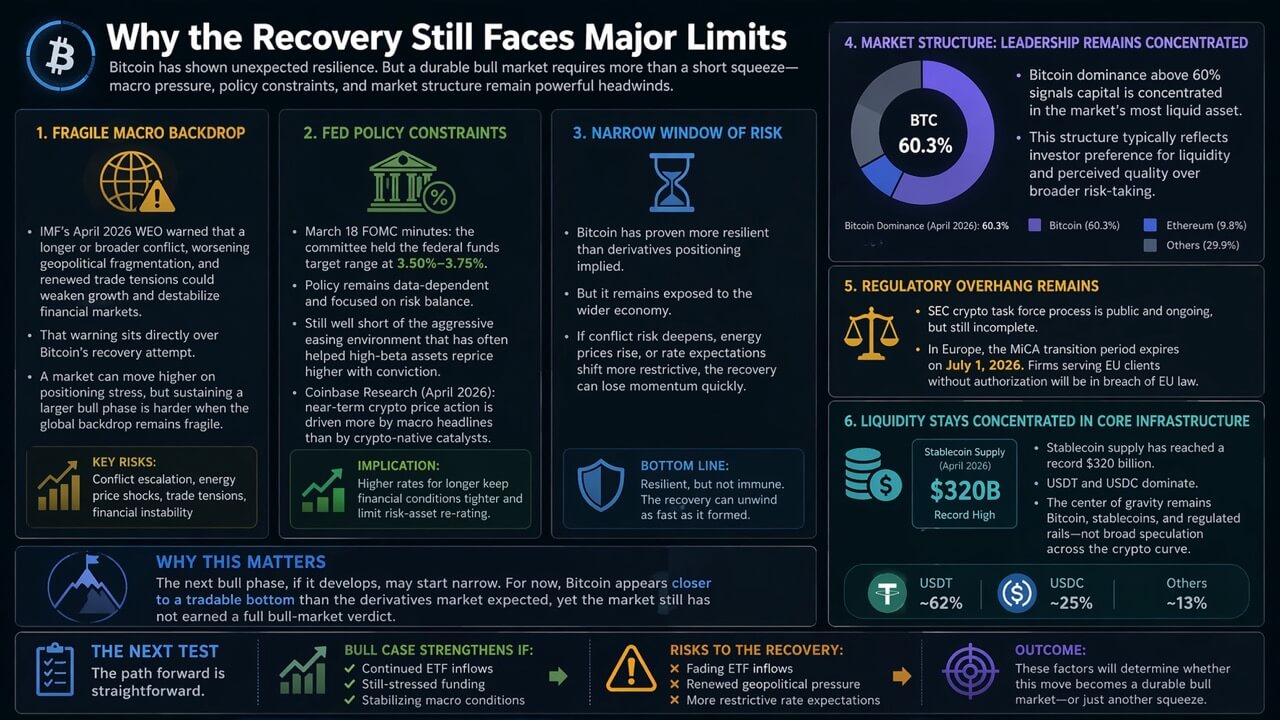

The IMF's April 2026 World Economic Outlook warned that a longer or broader conflict, worsening geopolitical fragmentation, and renewed trade tensions could significantly weaken growth and destabilize financial markets. That warning lands directly on top of Bitcoin's current recovery attempt.

A market can squeeze higher on positioning stress. Sustaining a broad bull phase is harder if the global macro backdrop continues to deteriorate.

The rates picture reinforces that ceiling. Minutes from the Federal Reserve's March 18 meeting showed the committee kept the federal funds target range at 3.5% to 3.75% and remained focused on incoming data and the balance of risks.

That is still far from the kind of aggressive easing cycle that has historically helped high-beta assets reprice higher with conviction. Coinbase Research reached a similar conclusion in its April outlook, arguing that near-term crypto price action was being driven more by macro headlines than by crypto-native catalysts.

That leaves Bitcoin in a narrow but important window. It looks more resilient than the derivatives market expected, but it does not yet look insulated from the wider economy.

If conflict risk worsens, if energy prices tighten financial conditions further, or if rate expectations move in a more restrictive direction, the recovery can still lose altitude quickly.

Why the next bull phase may start narrow

The structure of the broader crypto market also argues against calling an immediate full-spectrum bull market. Bitcoin's dominance above 60%, according to CryptoSlate'smarket data, suggests that leadership remains concentrated in the market's most liquid asset.

That usually happens when investors are favoring liquidity and perceived quality over broader risk. It fits the current environment and the policy backdrop.

The SEC's crypto task force page shows a regulatory process that is active, public, but still incomplete. In Europe, the MiCA transition period expires on July 1, 2026, after which firms serving EU clients without authorization will be in breach of EU law.

That is a more formal setting than the looser regulatory periods that powered earlier crypto rallies. The market is maturing, but under closer supervision.

At the same time, money within crypto continues to flow through the industry's plumbing. Stablecoin supply has climbed to a record $320 billion, with USDT and USDC dominating liquidity even as Washington continued to wrestle with market-structure legislation.

That proves the current crypto zeitgeist is still centered on Bitcoin, stablecoins, and regulated rails rather than on broad speculative breadth.

If a larger bull phase eventually develops, it may begin from that narrower base instead of arriving all at once across the risk curve.

For now, Bitcoin looks closer to a tradable bottom than the derivatives crowd expected, but the market has not yet earned a full bull-market verdict.

Alphractal's chart shows its sentiment Index plunging to extreme lows near several major Bitcoin troughs, indicating sentiment and positioning appear to be back in a historical capitulation zone rather than at an ordinary dip.

Still, a static chart can support the pattern qualitatively, but it is not precise enough on its own to verify the timing language for local bottoms forming within 21 days.

The next test is clear. If ETF inflows continue to build, if funding remains negative or only slowly normalizes, and if macro stress stabilizes, the case for a durable bottom strengthens.

If inflows fade or geopolitical and rate pressure intensify again, the current rebound will look more like a squeeze than the first leg of a new bull market.