Strategy's preferred stack and Bitcoin's price are facing two separate tests this week, and only one of them has been resolved.

The company's Digital Credit Capital Framework centers on a $2.55 billion dollar-denominated reserve, a revised STRC dividend policy, $2 billion in combined buybacks, and a board-authorized BTC monetization program.

MSTR rose roughly 6% in pre-market trading, and STRC climbed to about $81, still well off its $100 par value. The framework provides Strategy with a defined path to meet its dividend obligations without forced dilution or panic selling.

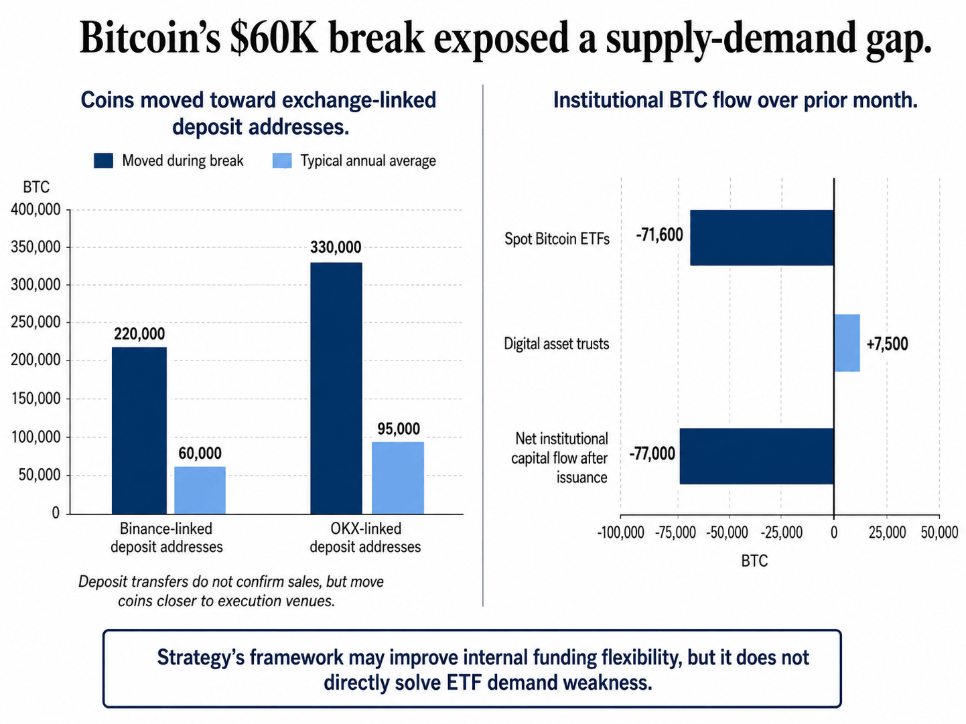

Spot ETFs shed roughly 71,600 BTC over the prior month, a demand gap that a corporate buyback program has no mechanism to close.

Strategy framework item

Size / detail

What it fixes

What it does not fix

Dollar reserve

$2.55B

Creates visible dividend and interest runway

Does not create BTC spot demand

Reserve coverage

17.4 months

Reduces panic around preferred obligations

Still below the longer 26-month runway including monetization capacity

Minimum reserve policy

12 months

Gives investors a policy floor

Does not eliminate need for future replenishment

STRC dividend

12%, up from 11.5%

Supports preferred-holder confidence

STRC still trades below $100 par

Combined buybacks

$2B

Gives management tools to support securities

Buybacks compete with reserve needs

BTC monetization authority

Up to $1.25B

Creates conditional liquidity source

Formalizes BTC as a sellable treasury asset

What Strategy fixed

Strategy's $2.55 billion-denominated reserve covers about 17.4 months of the company's roughly $1.76 billion in annual preferred dividend and interest obligations, with a board policy requiring at least 12 months' coverage.

The company raised STRC's dividend rate to 12% from 11.5%, effective for record dates after July 1, and set a monthly review process tied to trading levels, credit spreads, Bitcoin price and volatility, and reserve coverage.

Lacie Zhang, a research analyst at Bitget Wallet, said analysts had flagged that Strategy's cash reserves had shrunk to cover just 14 months of preferred dividend costs, with roughly $904 million in annual obligations against only about $150 million in software operating cash flow.

Zhang said:

“The funding gap is structural, not temporary. Rebuilding reserves to $2.55 billion and extending runway to 26 months buys time and restores credibility with preferred shareholders, particularly STRC holders who've watched the security trade 25% below its $100 par value.”

The program authorizes up to $1.25 billion in BTC sales for three purposes: rebuilding the dollar reserve, funding preferred dividends and interest when management decides selling Bitcoin beats issuing new equity, and financing the buyback programs.

Strategy holds 847,363 BTC at an aggregate purchase price of $64.1 billion, against a current Bitcoin price of around $60,000, roughly $16,000 below that average cost.

Zhang called this a shift from the company's long-held accumulate-and-never-sell posture. MSTR's pre-market gain reflected relief that the funding gap finally has an answer, even one that includes selling Bitcoin at a loss if conditions force it.

She noted:

“Strategy is managing Bitcoin as a treasury asset with real liquidity discipline, not just an ideological position. Whether that's good or bad depends on where Bitcoin goes next, which has always been the only question that matters here.”

Bitcoin's separate problem

Bitcoin's break below $60,000 exposed a market that had grown comfortable inside a narrow range since February.

CryptoQuant data show more than 220,000 BTC moved into Binance-linked deposit addresses and more than 330,000 BTC into OKX-linked deposit addresses after the break, compared with typical annual averages of 60,000 and 95,000 BTC, respectively.

Deposit-address transfers don't confirm sales, but they put coins closer to the venues where sales happen, right as the market's most-watched support level gave way.

Glassnode data shows spot Bitcoin ETFs lost about 71,600 BTC over the past month, while digital asset trusts added only about 7,500 BTC.

Adjusted for new issuance, the combined net institutional capital flow was around -77,000 BTC.

Strategy's framework lowers the odds that one of Bitcoin's largest corporate holders becomes a forced seller, a different constituency from the ETF buyers who pulled back when $60,000 broke and have stayed away since.

Options traders have built downside protection concentrated around $55,000 to $58,000 for July expiry, with roughly $1.2 billion in open interest clustered at the $55,000 and $50,000 strikes on Deribit, a setup that cuts in either direction.

A $60,000 reclaim would force those hedges to unwind and could amplify a rebound. A failed reclaim turns the put-heavy zone into the market's next test, exactly where positioning already expects it to go.

A two-panel chart shows Bitcoin exchange deposit inflows exceeding annual averages after the $60,000 break, alongside spot ETFs losing 71,600 BTC over the prior month.

Two ways this breaks

The bull case needs four things moving together: Bitcoin reclaiming and holding $60,000; ETF flows turning positive after a month of outflows; exchange-linked transfers that spiked after the break cooling back toward historical averages; and STRC closing the gap toward its $100 par value as confidence in Strategy's framework builds.

A reclaim without ETF demand would still leave a fragile setup, with a supply overhang sitting close enough to execution venues to cap any rally.

The bear case is BTC failing to hold $60,000, which turns the level into resistance and moves attention to the $55,000 to $58,000 zone, where July puts are already concentrated. Continuing ETF outflows would confirm institutional demand is staying on the sidelines regardless of what Strategy resolves.

Exchange-linked inflows staying elevated would keep sellable supply close to the market, and Strategy's BTC monetization authority, conditional as it is, formalizes Bitcoin as a liquidity source for the first time in the company's history.

June CPI lands on July 14 and still carries the imprint of the oil-shock period, so neither case gets resolved by that print alone.

Scenario

What has to happen

Confirmation signal

Failure signal

Bull case: recovery from $60K

BTC reclaims and holds $60,000; ETF flows turn positive; exchange-linked transfers cool; STRC moves closer to par

$60K becomes accepted support and July downside hedges begin to unwind

$55K-$58K becomes the next live test as put positioning takes over

ETF buyers return or exchange flows normalize

Macro delay case

June CPI is noisy, leaving traders waiting for July CPI and July PCE

Market stays range-bound and flow-driven until August data

Hot inflation or oil-risk revival pushes real-rate pressure higher

Strategy-risk case

STRC remains far below par or reserve pressure returns

Market starts pricing BTC monetization as more likely

STRC improves and the reserve backstop gains credibility

July CPI on Aug. 12 is the first genuinely cleaner read on inflation, the OFAC oil-license window expires Aug. 21, and July PCE on Aug. 26 gives the Fed's preferred inflation gauge its first clean look since the shock began. Bitcoin trades on positioning and flows until those prints land.

Strategy closed the risk that one of crypto's largest corporate balance sheets becomes a forced seller without warning.

The headwind that stays belongs to Bitcoin alone: buyers returning at a scale that outweighs 550,000 BTC sitting near exchange deposit addresses and a month of ETF outflows still working their way through the market.