Strategy (formerly MicroStrategy) shares rose Monday after the Bitcoin holder moved to reassure investors that it can meet its preferred stock obligations, authorizing up to $2 billion in buybacks and opening the door to Bitcoin sales that could fund dividends, interest payments, and repurchases.

The company, led by Executive Chairman Michael Saylor, announced a new Digital Credit Capital Framework that gives management more room to defend its capital structure, which has come under pressure as Bitcoin weakened and Strategy’s preferred securities traded below their stated values.

Following the announcement, MSTR gained 3.9% to $85.52 in early market trading, while the distressed STRC climbed to $81.

These price actions followed a broader sell-off in these stocks last week, when investors questioned whether Strategy could continue to rely on equity and preferred stock issuance to fund its Bitcoin strategy without adding pressure on existing shareholders.

The framework marks one of the clearest signs yet that Strategy is adjusting its playbook after years of raising capital to accumulate Bitcoin.

The company said it remains committed to Bitcoin as its primary treasury reserve asset, but it now has formal authority to use part of that reserve as a source of liquidity when management decides that selling Bitcoin is more attractive than issuing common stock or other securities.

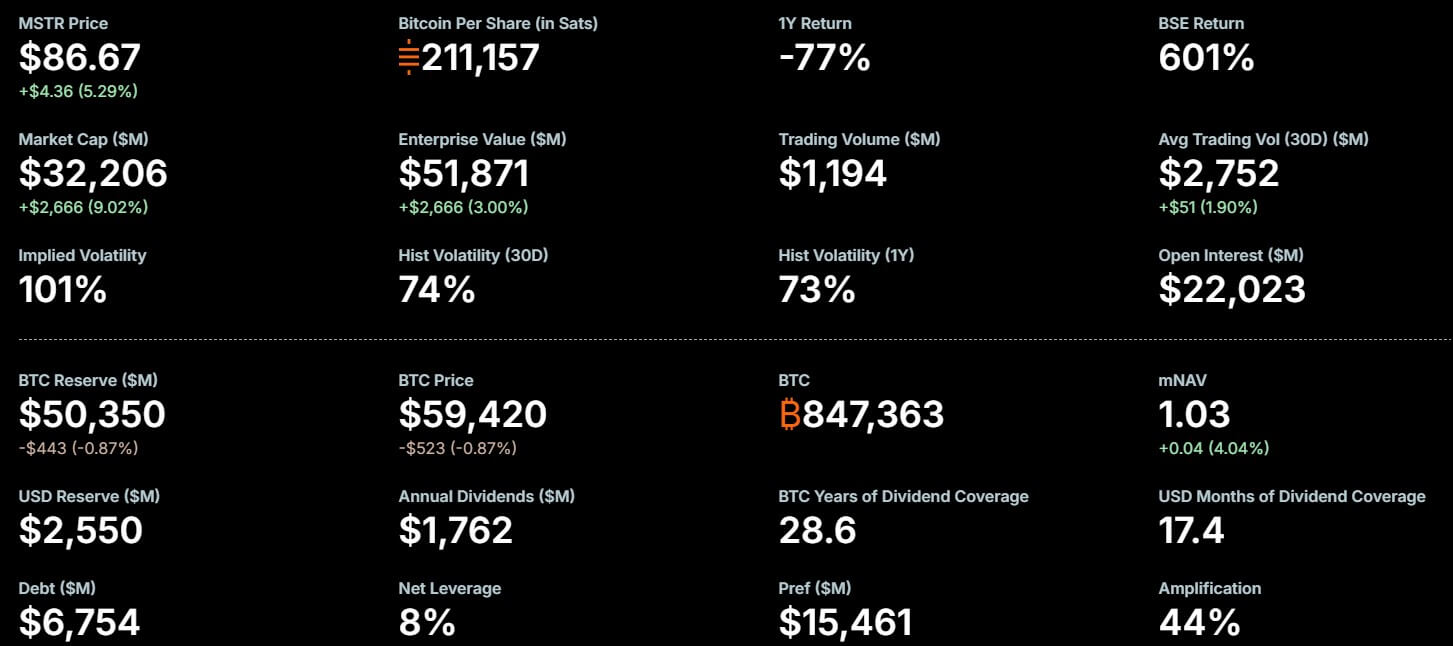

Strategy held 847,363 Bitcoin as of June 28, valued at about $50.7 billion. The position remains the largest corporate Bitcoin holding in public markets, but it also carries an unrealized loss of more than $13 billion based on the company’s disclosed acquisition cost.

Strategy builds cash reserve

Strategy said its US dollar reserve stood at about $2.55 billion as of June 28, including expected proceeds from shares sold through its at-the-market offering program that had not yet settled.

The company said the reserve may be used only to pay dividends on preferred stock and interest on outstanding debt unless the board approves another use. Based on current annual preferred dividend payments and interest expense of about $1.76 billion, the reserve provides coverage of about 17.4 months.

Strategy Key Metrics (Source: Strategy)

The board also adopted a policy requiring Strategy to maintain a minimum reserve equal to at least 12 months of expected preferred dividends and interest expense. Any move below that threshold would require board approval.

That reserve is intended to address one of the central concerns around Strategy’s funding model. Its Bitcoin holdings do not generate income, whereas the preferred securities issued to finance the company’s Bitcoin accumulation carry recurring dividend obligations.

The company also said it has $1.25 billion of board-authorized Bitcoin monetization capacity that can be used to build or replenish the reserve.

When combined with the current cash reserve, Strategy said it has about $3.8 billion of current liquidity coverage for preferred dividends and interest expense, equal to 25.9 months of coverage before repurchases, taxes, transaction costs, market conditions or changes in dividend rates.

STRC dividend rises to 12%

Strategy also raised the annual dividend rate on its Variable Rate Series A Perpetual Stretch Preferred Stock, known as STRC, to 12% from 11.5%. The increase applies to semi-monthly periods with record dates on or after July 1.

The security was trading around $81 at press time, leaving it at a deep discount to par despite the company’s stated objective of bringing it back toward the $99-$100 range over time.

The company said it will review the STRC dividend rate monthly, using factors including the security’s trading level, market yields, credit spreads, Bitcoin price and volatility, reserve coverage and broader capital market conditions.

Strategy also cautioned that it will not automatically raise the STRC dividend simply because the security trades below its stated amount. Dividends remain subject to board approval and are not guaranteed.

That distinction is important for investors who have treated STRC as a test of confidence in Strategy’s Bitcoin-backed credit model.

The higher payout may help narrow the discount, but it also increases the cost of keeping the preferred stock complex stable if market yields continue to rise or Bitcoin remains weak.

Speaking on the move, Quinn Thompson, Chief Investment Officer at Lekker Capital, viewed the announcement as a necessary response to recent market duress.

Thompson noted that Strategy's common stock had declined nearly 30% in the preceding week, indicating elevated selling pressure. He characterized the decision to funnel recent equity offering proceeds directly into a defensive cash reserve as a highly positive development for institutional confidence.

However, Thompson expressed skepticism that a 50-basis-point dividend increase alone would be sufficient to drive STRC back to its $100 par value, though he acknowledged that the firm's overall capital structure has been significantly stabilized by the presence of a definitive, multi-billion-dollar backstop.

The company said STRC is expected to be the program's initial focus if management determines that repurchases would be accretive and strengthen the capital structure.

Repurchases may take place through open-market purchases, block trades, tender offers, exchange offers or privately negotiated transactions.

The authorization does not require Strategy to buy any specific amount of securities and has no fixed expiration date.

The logic is straightforward. If Strategy buys preferred securities at a significant discount to their stated amount, it can reduce future dividend obligations while potentially improving confidence in the remaining securities.

That could help the company lower the cost of supporting its capital structure, though it would also require cash or Bitcoin sales if funded outside regular capital markets activity.

Strategy also authorized a separate $1 billion repurchase program for its Class A common stock. The company said common stock buybacks may be used when management believes MSTR is trading below intrinsic value.

Neither preferred nor common stock repurchases will be funded from the US dollar reserve, the company said. If Strategy uses Bitcoin sales to fund repurchases, those sales would fall under the Bitcoin monetization program.

Chief Executive Officer Phong Le said the company is shifting from a model centered on issuing securities to one that also uses repurchases when market prices make them attractive. He added:

“We intend to move between issuing securities when capital is attractive and repurchasing securities when our instruments trade at levels that make buybacks accretive.”

Bitcoin becomes part of liquidity plan

The Bitcoin monetization program is the most significant part of the framework for long-term Strategy investors.

Under the program, the company may sell Bitcoin for three purposes: to generate up to $1.25 billion for the US dollar reserve, to fund or replenish cash used for preferred dividends and interest expense, and to finance repurchases of Digital Credit Securities or MSTR common stock.

The program has no fixed expiration date and does not require Strategy to sell Bitcoin. Any sale would depend on market conditions, liquidity needs, taxes, accounting issues, legal requirements, and management’s assessment of shareholder value.

Still, the authorization formalizes a shift that had already begun. Strategy sold 32 Bitcoins for about $2.5 million between May 26 and May 31, only the second known Bitcoin sale in the company’s history.

That sale was small compared with the company’s overall holdings, but it signaled a willingness to use Bitcoin as a balance sheet tool when management believes doing so can improve its financial position.

The new framework expands that flexibility.

For years, Saylor’s strategy relied on turning public market demand for MSTR and related securities into a funding engine for Bitcoin purchases.

That model worked best when MSTR traded at a large premium to the value of its Bitcoin holdings, allowing the company to sell equity or preferred instruments and use the proceeds to buy more Bitcoin in a way management described as accretive.

That premium has narrowed sharply. Strategy said it expects to remain disciplined in its use of common equity issuance, especially when MSTR trades at or near 1x mNAV per share, a valuation measure tied to the company’s Bitcoin holdings.

The new framework gives management another path. Instead of relying mainly on new issuance, Strategy can use cash reserves, Bitcoin monetization, and buybacks to manage the liabilities created by its own capital raising.

Despite the new possibility of BTC selling, Saylor said:

Strategy remains committed to Bitcoin as its primary treasury reserve asset. At the same time, Digital Credit requires liquidity, discipline, and active capital management.