US crypto perps are live but Bitcoin may be the only market many traders can actually useKalshi’s live U.S.-regulated crypto perpetual futures move the story out of the approval phase and into the order book.

The company’s public perpetual futures page and individual product pages now present U.S.-regulated crypto perps as a broader trading category that extends past the first Bitcoin experiment.

Kalshi’s own materials point to markets across Bitcoin, Ethereum, Solana, XRP, and other crypto assets, while a dedicated HYPE perpetual page shows the company has extended the product into one of the assets most closely associated with demand for crypto-native derivatives.

The launch changes the test from permission to behavior. Traders will compare spreads, depth, funding, reference prices, collateral workflow, fees, APIs, leverage, and whether market makers continue to quote when volatility rises.

Bitcoin enters that test with the clearest advantage because it has the deepest spot footprint and the most familiar benchmark infrastructure. The altcoin markets could become relevant, but each one has to earn that status one order book at a time.

Approval Starts The Market Test

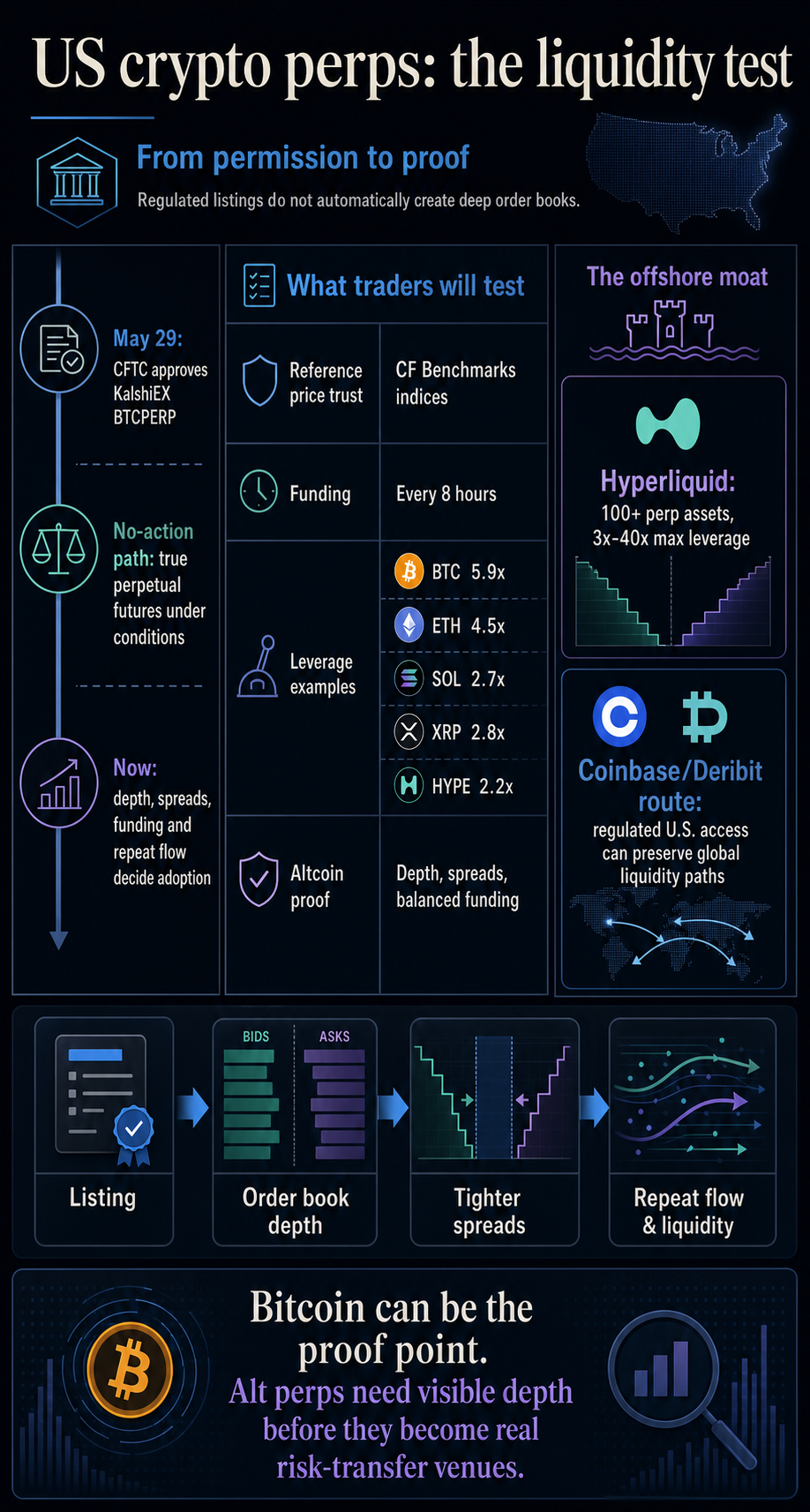

The legal opening is real; adoption is a separate problem. The CFTC approved KalshiEX’s BTCPERP contract on May 29 as a futures contract referencing the spot price of Bitcoin.

The agency later issued additional no-action context for designated contract markets converting certain existing digital commodity perpetual-style futures into true perpetual futures, subject to customer-protection and procedural conditions.

That regulatory path makes the products possible. It does not supply counterparties, market makers, or a track record of execution quality during volatile sessions.

Kalshi’s product mechanics show why liquidity will be hard-earned. Its explainer says funding is charged every 8 hours, and its June 3 leverage examples varied materially by asset: Bitcoin at 5.9x, Ethereum at 4.5x, Solana at 2.7x, XRP at 2.8x, and HYPE at 2.2x.

Its help center says all Kalshi crypto perps use CF Benchmarks indices for funding and settlement reference pricing, with Bitcoin tied to the Bitcoin Real Time Index.

Those mechanics set the conditions for adoption. A reference price affects confidence around funding and liquidations. Leverage limits shape the type of trader the product attracts.

Minimum order sizes influence whether a market feels usable for smaller active traders or mainly for larger positions. For non-BTC contracts, those details are included in the first liquidity screen.

A real market should show tight spreads, durable two-sided books, and volume that holds after launch attention fades. It should also show funding behavior that remains orderly when sentiment leans heavily toward either the long or the short.

Those execution signals now carry more weight than another full legal recap. Small frictions can quickly decide whether active traders return.

The legal fight has already been detailed, including the earlier approval process and the CME challenge. Market behavior will decide the next phase: where depth forms, where spreads tighten, and where active traders keep returning.

Bitcoin Has The Clearest Path To Depth

Bitcoin is the easiest asset for regulated U.S. perps to organize around. CryptoSlate’s Bitcoin market data showed a far larger 24-hour spot volume than that of the major alt assets in its market set, while the broader crypto market page showed Bitcoin’s dominant share.

Those figures are in a broad spot-market context rather than the Kalshi venue volume, but they explain why Bitcoin is the natural first anchor for a regulated perp venue.

A perp contract depends on more than a symbol. It needs a reference price traders trust, sufficient spot liquidity for arbitrage and hedging, and sufficient flow on both sides to prevent funding from becoming one-sided.

Bitcoin is best positioned, based on the available evidence, because it has the largest market footprint and the clearest institutional benchmark context.

That same logic raises the bar for altcoin adoption. Ethereum, Solana, XRP, and HYPE can be listed, and Kalshi’s materials support a broad asset set across its help center, explainer, and product pages.

Listing an alt market starts the tryout; sustained depth, spread quality, and balanced funding decide whether it becomes a primary risk-transfer venue.

Each alt market has a different burden. Ethereum has deeper market infrastructure than most crypto assets, but it still competes with entrenched offshore and crypto-native derivatives venues.

Solana and XRP have large spot-market profiles, but their perp liquidity depends on whether professional traders see enough consistent depth to justify routing flow.

HYPE is more unusual because its token is tied closely to the Hyperliquid ecosystem, whose own docs describe broad perp asset coverage and leverage ranges beyond Kalshi’s date-stamped examples.

HYPE gives Kalshi a timely asset tied directly to the derivatives narrative. It also highlights the competitive problem: Hyperliquid’s documented perp surface gives traders a familiar crypto-native benchmark for asset coverage and leverage.

Venue habit is the inference to watch, while actual migration toward Kalshi still needs visible depth and spread data.

Offshore Venues Still Own Trader Habit

The global perp market is already large and deeply habituated. CoinGecko’s 2026 perpetuals report framed crypto perps as a massive global derivatives category, with centralized exchanges still accounting for most open interest.

Hyperliquid’s own materials describe more than 100 perpetual assets and 3x-40x max leverage, giving crypto-native traders a product surface broader and more aggressive than the early U.S.-regulated examples.

Offshore and crypto-native venues can still be challenged. Regulated U.S. routes have a cleaner compliance story for traders who want onshore access, and that can carry weight.

The competition now shifts to execution quality, product coverage, collateral workflow, APIs, fees, and whether market makers see enough repeat flow to quote aggressively.

Coinbase adds another wrinkle. The CFTC’s May 29 interpretation and no-action position for Coinbase Financial Markets concerned access to Deribit products through a regulated U.S. futures commission merchant.

Coinbase’s own announcement described that route as a way for U.S. clients to access global crypto perps and options without offshore workarounds.

That route may preserve some existing global liquidity patterns instead of forcing all new U.S. demand into domestic order books. That arrangement supports the access-path implication without proving actual flow movement.

Regulated access can mean a new onshore listing venue or a regulated gateway to products connected to existing global derivatives infrastructure.

For traders, the choice will be practical. They will compare spread, depth, funding history, fees, available leverage, collateral mechanics, order types, reliability, and asset coverage.

If Kalshi’s Bitcoin perp becomes easy to trade with low friction and dependable two-sided liquidity, Bitcoin could become the proof point for regulated U.S. crypto perps. If the alt markets remain thin or expensive to trade, the broader board could function more like optional coverage than real liquidity migration.

The test is measurable. Monitor whether Bitcoin continues to dominate the volume mix even as more assets emerge. Watch whether HYPE, SOL, and XRP spreads stay competitive during volatile sessions.

Watch whether funding remains orderly or becomes a tax on one crowded side of the trade. Watch whether market makers keep quoting outside Bitcoin after launch incentives fade. And watch whether traders use the venue when volatility spikes, because that is when liquidity claims face their real test.

U.S.-regulated perps now have the permission they lacked. The market still has to show whether they can become a habit. For now, the evidence supports a Bitcoin-first hypothesis where alt perps are real listings, while durable non-BTC liquidity centers still need evidence.

The post appeared first on CryptoSlate.

read the full story

Kalshi’s live U.S.-regulated crypto perpetual futures move the story out of the approval phase and into the order book.

The company’s public perpetual futures page and individual product pages now present U.S.-regulated crypto perps as a broader trading category that extends past the first Bitcoin experiment.

Kalshi’s own materials point to markets across Bitcoin, Ethereum, Solana, XRP, and other crypto assets, while a dedicated HYPE perpetual page shows the company has extended the product into one of the assets most closely associated with demand for crypto-native derivatives.

The launch changes the test from permission to behavior. Traders will compare spreads, depth, funding, reference prices, collateral workflow, fees, APIs, leverage, and whether market makers continue to quote when volatility rises.

Bitcoin enters that test with the clearest advantage because it has the deepest spot footprint and the most familiar benchmark infrastructure. The altcoin markets could become relevant, but each one has to earn that status one order book at a time.

Approval Starts The Market Test

The legal opening is real; adoption is a separate problem. The CFTC approved KalshiEX’s BTCPERP contract on May 29 as a futures contract referencing the spot price of Bitcoin.

The agency later issued additional no-action context for designated contract markets converting certain existing digital commodity perpetual-style futures into true perpetual futures, subject to customer-protection and procedural conditions.

That regulatory path makes the products possible. It does not supply counterparties, market makers, or a track record of execution quality during volatile sessions.

Kalshi’s product mechanics show why liquidity will be hard-earned. Its explainer says funding is charged every 8 hours, and its June 3 leverage examples varied materially by asset: Bitcoin at 5.9x, Ethereum at 4.5x, Solana at 2.7x, XRP at 2.8x, and HYPE at 2.2x.

Its help center says all Kalshi crypto perps use CF Benchmarks indices for funding and settlement reference pricing, with Bitcoin tied to the Bitcoin Real Time Index.

Those mechanics set the conditions for adoption. A reference price affects confidence around funding and liquidations. Leverage limits shape the type of trader the product attracts.

Minimum order sizes influence whether a market feels usable for smaller active traders or mainly for larger positions. For non-BTC contracts, those details are included in the first liquidity screen.

A real market should show tight spreads, durable two-sided books, and volume that holds after launch attention fades. It should also show funding behavior that remains orderly when sentiment leans heavily toward either the long or the short.

Those execution signals now carry more weight than another full legal recap. Small frictions can quickly decide whether active traders return.

The legal fight has already been detailed, including the earlier approval process and the CME challenge. Market behavior will decide the next phase: where depth forms, where spreads tighten, and where active traders keep returning.

Bitcoin Has The Clearest Path To Depth

Bitcoin is the easiest asset for regulated U.S. perps to organize around. CryptoSlate’s Bitcoin market data showed a far larger 24-hour spot volume than that of the major alt assets in its market set, while the broader crypto market page showed Bitcoin’s dominant share.

Those figures are in a broad spot-market context rather than the Kalshi venue volume, but they explain why Bitcoin is the natural first anchor for a regulated perp venue.

A perp contract depends on more than a symbol. It needs a reference price traders trust, sufficient spot liquidity for arbitrage and hedging, and sufficient flow on both sides to prevent funding from becoming one-sided.

Bitcoin is best positioned, based on the available evidence, because it has the largest market footprint and the clearest institutional benchmark context.

That same logic raises the bar for altcoin adoption. Ethereum, Solana, XRP, and HYPE can be listed, and Kalshi’s materials support a broad asset set across its help center, explainer, and product pages.

Listing an alt market starts the tryout; sustained depth, spread quality, and balanced funding decide whether it becomes a primary risk-transfer venue.

Each alt market has a different burden. Ethereum has deeper market infrastructure than most crypto assets, but it still competes with entrenched offshore and crypto-native derivatives venues.

Solana and XRP have large spot-market profiles, but their perp liquidity depends on whether professional traders see enough consistent depth to justify routing flow.

HYPE is more unusual because its token is tied closely to the Hyperliquid ecosystem, whose own docs describe broad perp asset coverage and leverage ranges beyond Kalshi’s date-stamped examples.

HYPE gives Kalshi a timely asset tied directly to the derivatives narrative. It also highlights the competitive problem: Hyperliquid’s documented perp surface gives traders a familiar crypto-native benchmark for asset coverage and leverage.

Venue habit is the inference to watch, while actual migration toward Kalshi still needs visible depth and spread data.

Offshore Venues Still Own Trader Habit

The global perp market is already large and deeply habituated. CoinGecko’s 2026 perpetuals report framed crypto perps as a massive global derivatives category, with centralized exchanges still accounting for most open interest.

Hyperliquid’s own materials describe more than 100 perpetual assets and 3x-40x max leverage, giving crypto-native traders a product surface broader and more aggressive than the early U.S.-regulated examples.

Offshore and crypto-native venues can still be challenged. Regulated U.S. routes have a cleaner compliance story for traders who want onshore access, and that can carry weight.

The competition now shifts to execution quality, product coverage, collateral workflow, APIs, fees, and whether market makers see enough repeat flow to quote aggressively.

Coinbase adds another wrinkle. The CFTC’s May 29 interpretation and no-action position for Coinbase Financial Markets concerned access to Deribit products through a regulated U.S. futures commission merchant.

Coinbase’s own announcement described that route as a way for U.S. clients to access global crypto perps and options without offshore workarounds.

That route may preserve some existing global liquidity patterns instead of forcing all new U.S. demand into domestic order books. That arrangement supports the access-path implication without proving actual flow movement.

Regulated access can mean a new onshore listing venue or a regulated gateway to products connected to existing global derivatives infrastructure.

For traders, the choice will be practical. They will compare spread, depth, funding history, fees, available leverage, collateral mechanics, order types, reliability, and asset coverage.

If Kalshi’s Bitcoin perp becomes easy to trade with low friction and dependable two-sided liquidity, Bitcoin could become the proof point for regulated U.S. crypto perps. If the alt markets remain thin or expensive to trade, the broader board could function more like optional coverage than real liquidity migration.

The test is measurable. Monitor whether Bitcoin continues to dominate the volume mix even as more assets emerge. Watch whether HYPE, SOL, and XRP spreads stay competitive during volatile sessions.

Watch whether funding remains orderly or becomes a tax on one crowded side of the trade. Watch whether market makers keep quoting outside Bitcoin after launch incentives fade. And watch whether traders use the venue when volatility spikes, because that is when liquidity claims face their real test.

U.S.-regulated perps now have the permission they lacked. The market still has to show whether they can become a habit. For now, the evidence supports a Bitcoin-first hypothesis where alt perps are real listings, while durable non-BTC liquidity centers still need evidence.

The post appeared first on CryptoSlate.

read the full storyDid Scott Bessent Just Call The Bottom Of The Bitcoin Bear Market?

Bitcoin just broke below 60K, the bears are celebrating, and the loudest skeptics are calling for…

Bitcoin Slides Toward $58,000 As ETF Outflows And Options Expiry Add Pressure

Bitcoin and the wider crypto market faced a heavy risk-off session as ETF redemptions, leverage…

Will Bitcoin (BTC) Return to $60,000? XRP's Risks of Losing $1, Shiba Inu's (SHIB) Bearish Pressure Is Weakening: Crypto Market Review

Some levels are already toxic for assets like XRP and Shiba Inu, the worst part is that it might…

Tether Briefly Overtakes Ethereum As Stablecoin Market Cap Tops ETH During Sell-Off

Tether briefly moved above Ethereum by market capitalization during a sharp ETH drawdown, marking a…

Metaplanet bets Bitcoin treasury firms can survive by packaging Bitcoin income

Regulated securities rails could give BTC treasury firms a new engine, if product demand and mNAV…

Bitcoin price prediction: Is the four-year cycle dead, or just running late?

Bitcoin sits near $60,000, down more than half from its October peak, with traders in extreme fear…

Ripple Launches RLUSD in Japan via SBI as Circle and Nomura Join Stablecoin Race

Ripple's RLUSD stablecoin went live in Japan on Tuesday after receiving approval from Japan's…

Bitcoin Bounces Back Above $60K as $10.6 Billion Options Expiry Hits Deribit and CME

Bitcoin clawed back above $60,000 on Sunday after sliding near $58,000 overnight. The bounce came…

CryptoQuant CEO Warns Bitcoin Bottom Is Still Ahead

TL;DR CryptoQuant CEO Ki Young Ju states that Bitcoin’s cycle bottom is still not confirmed, based…

Crypto Traders Push BTC Near $60K as 30% YTD Decline Keeps 2026 Bear Market in Focus

Bitcoin snapped a two-day, $4,500 slide on Friday, experiencing choppy trading between $58,500 and…

Aave, Solana ecosystem tokens lead crypto rebound as bitcoin steadies near $60,000

Tokenized stock trading fueled fresh momentum across the Solana ecosystem, while Aave founder hinted…

British Billionaire: Bitcoin Will Die With a 'Whimper'

Legendary British billionaire investor and GMO co-founder Jeremy Grantham has leveled a scathing…

StablecoinX Begins Nasdaq Trading as First Public ENA Treasury Vehicle

StablecoinX Inc. (Nasdaq: USDE) began trading Friday after closing its SPAC merger with TLGY…

Ripple CTO David Schwartz Clarifies XRP And Bitcoin Origins In Timeline Debate

Ripple CTO Emeritus David Schwartz pushed back on claims that XRP predates Bitcoin, separating…

Fed Official Kashkari Gives Rate Hike Warning: How Will US Stocks and Bitcoin React?

The Kashkari rate hike call for 2026 and a sticky services inflation warning weigh on US stocks and…

Bitcoin Faces Divergent Views: Grantham Predicts Decline, Salinas Pliego Bets Big

Bitcoin is experiencing a truly peculiar period. On one hand, Jeremy Grantham, Wall Street’s…

'Just a Matter of Time': Bloomberg Predicts Tether Will Flip Bitcoin

Bloomberg Intelligence senior macro strategist Mike McGlone is convinced that it is "just a matter…