Strategy’s Bitcoin holdings have fallen roughly $12 billion below their purchase cost, placing the company’s capital-raising model under its sharpest pressure since it accelerated its Bitcoin treasury strategy.

The company held 847,363 Bitcoin as of June 21, acquired for an aggregate $64.1 billion at an average price of $75,651. With the top crypto recently trading near $60,000 to $62,000, the position was worth about $52 billion.

While this substantial unrealized loss does not compel Strategy to sell its holdings or create an automatic margin call, it significantly weakens the conditions that allowed the company to repeatedly issue securities, buy more Bitcoin, and expand a treasury that became central to its market valuation.

Strategy’s accumulation model has worked most efficiently when its common shares traded at a premium to the value of the Bitcoin on its balance sheet. That premium allowed the company to raise capital through stock sales while limiting the number of new shares issued.

As Bitcoin and Strategy’s stock have declined, that advantage has narrowed. The pressure has since spread to STRC, the company’s variable-rate perpetual preferred stock, which is trading well below the $100 stated amount Strategy designed it to track.

Preferred Shares Fall Further Below Target

Strategy created STRC as an income-oriented security intended to trade near its stated $100 price. The company can reset its dividend rate monthly to influence investor demand and support the market price.

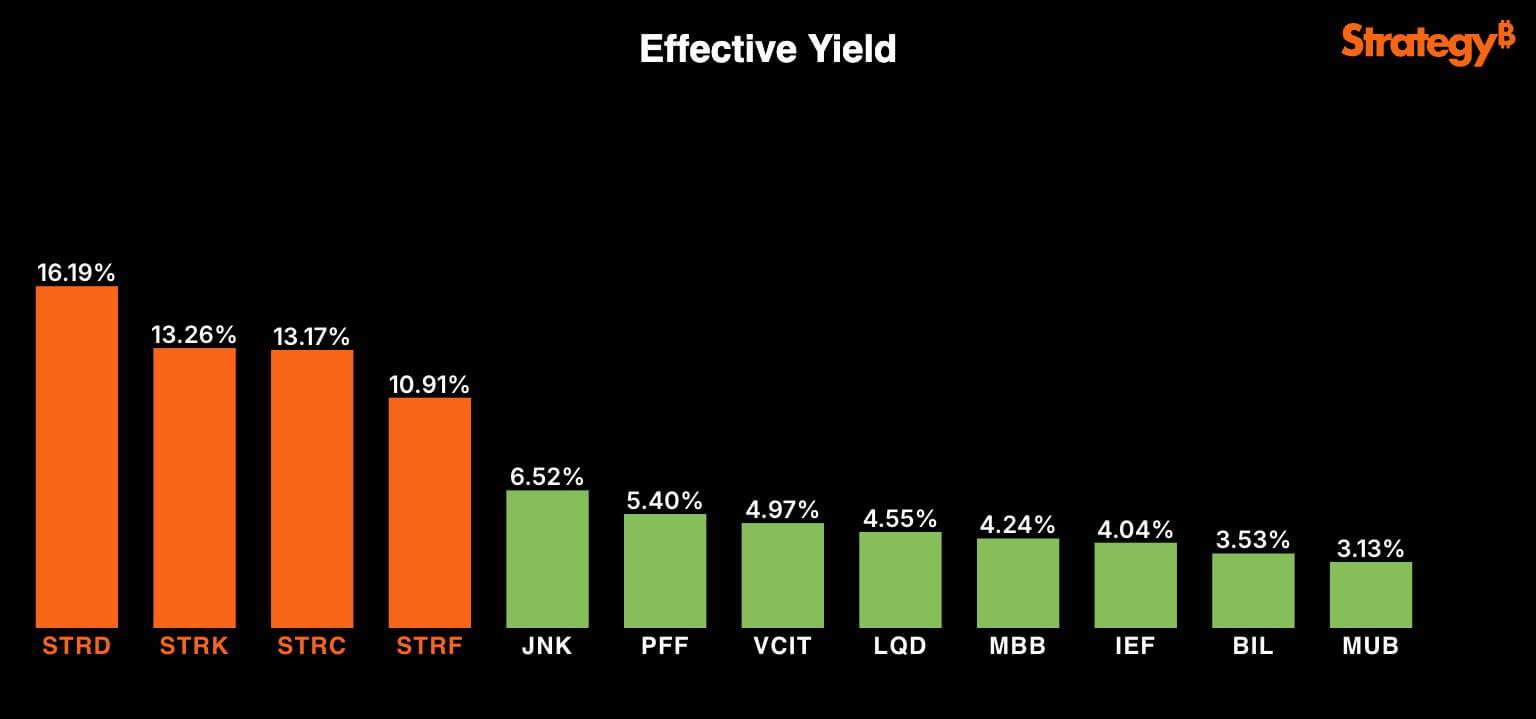

The security currently pays an annual dividend of 11.5%, equal to $11.50 per share based on the stated amount. STRC has nevertheless fallen to about $81, almost 20% below the level the company seeks to maintain.

At $81, the current payment represents an effective annual yield of about 14.2% for a new buyer, assuming Strategy’s board continues to declare the dividends and the rate remains unchanged.

The lower share price does not increase the amount Strategy pays on its existing STRC shares. It does show that investors are demanding a larger return to hold the security, and makes additional preferred-stock issuance less efficient.

Strategy could raise the dividend rate to encourage buying and help move STRC closer to $100. However, such an adjustment would add to the company’s recurring cash requirements. Meanwhile, keeping the rate unchanged would preserve liquidity but could leave the preferred stock trading at a persistent discount.

That trade-off has become more consequential as concerns over Strategy’s Bitcoin exposure and cash needs increase. The company has about $10.5 billion of STRC outstanding, meaning that even a modest rate increase could materially increase its annual dividend expense.

A sustained discount could also weaken STRC's ability to raise future financing. New investors may be unwilling to purchase additional shares near the stated amount while comparable securities trade substantially below it in the secondary market.

STRC options traders prepare for a wider range

The STRC options market shows traders positioning for both a partial recovery and further declines.

Total options volume reached about 10,400 contracts, or 167% of the average daily volume of 6,220. The volume put-call ratio stood at 1.35, meaning put activity exceeded call volume during the measured period.

The ratio points to a defensive tilt but does not show whether the puts were purchased or sold. Open-interest data also do not identify whether the positions belong to institutions, individual investors, or market makers.

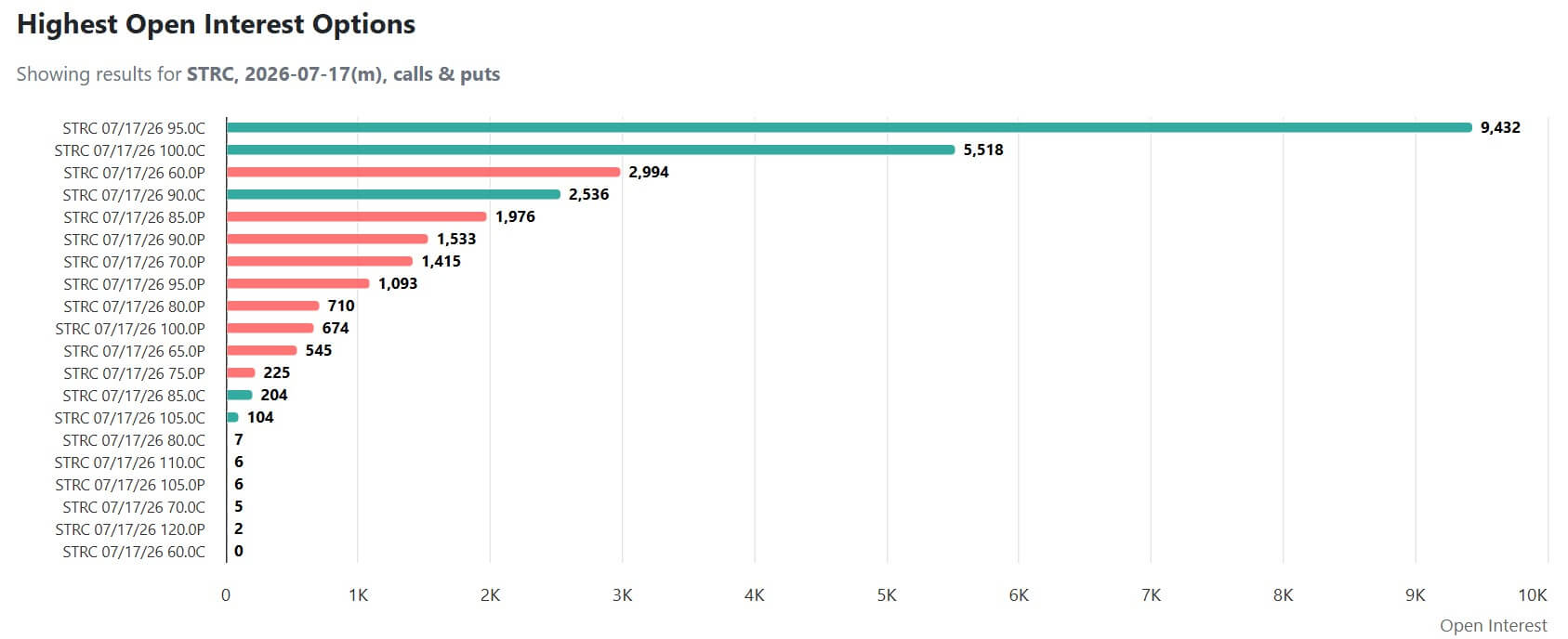

For contracts expiring on July 17, the largest concentration of open interest is in the $95 call, with 9,432 contracts outstanding. The $100 call carries another 5,518 contracts, while the $90 call has 2,536.

The concentration identifies the area between $95 and $100 as the principal upside range reflected in the options chain. A move toward those strikes would bring STRC closer to the level Strategy intended it to track.

STRC Options Trading (Source: Optionchart)

However, the positions do not establish that traders collectively expect such a recovery. Some of the calls may represent outright bullish bets, while others may have been sold against existing STRC holdings or used in multi-leg spreads that treat the region around $100 as an upper boundary.

Meanwhile, the downside positions extend considerably further.

Open interest includes 1,533 contracts at the $90 put, 1,976 at the $85 put, and 2,994 at the $60 put. The $60 strike would place STRC 40% below its stated amount and increase the effective yield to more than 19% if the current dividend rate were maintained.

These numbers show that some traders are preparing for a scenario in which the dividend-reset mechanism fails to restore the stock to $100 and investors continue to demand a larger return.

Taken together, the options positions define the range investors are watching. Calls near $95 and $100 preserve the possibility of a managed recovery.

However, the put positions, particularly at $60, show that traders are also protecting against a substantially larger discount.

Strategy builds cash and opens the door to Bitcoin sales

To navigate this market downturn, Strategy’s recent capital allocation suggests the company is placing greater emphasis on liquidity.

This week, the company announced that it raised about $335.5 million through common-stock sales, but used only $34.9 million to acquire 520 additional Bitcoins.

This action shows that the company is still acquiring Bitcoin, but cash needed for interest and preferred-dividend payments is competing more directly with additional purchases.

That marks a change from periods when the company directed a larger share of its available capital toward expanding the treasury.

Meanwhile, Strategy has also shown a willingness to sell some of its holdings to fund its operations.

Last month, Strategy sold 32 Bitcoin for about $2.5 million and said the proceeds were expected to help fund STRC distributions. This was Strategy’s first net Bitcoin disposal since 2022.

While the sale was negligible relative to the size of the company’s holdings, it demonstrated that part of the treasury could be converted into cash when other financing channels became less attractive.

Speaking on this action, Ki Young Ju, CryptoQuant CEO, said:

“[Strategy needs to] create a disciplined selling framework for the next bull market. Partial sales near cycle highs would not mean abandoning Bitcoin. It would deleverage the company, realize shareholder value, and create dry powder to re-accumulate lower. That's not trading. It's risk management”

Strategy Has Time, but Fewer Easy Choices

The overall pressure on Strategy and STRC has divided market observers over whether the Saylor-led firm is confronting a temporary loss of confidence or a deeper flaw in its financing model.

Su Zhu, the co-founder of the defunct Three Arrows Capital, argued that the preferred stock could stabilize as shares pass from shorter-term investors to holders more willing to accept its elevated yield and volatility. In his view, Strategy may not need an immediate overhaul if stronger demand emerges at the lower price.

He said the company could further support confidence by explaining how STRC holders would be treated if dividends were suspended, including whether the shares might eventually carry a claim on Strategy’s Bitcoin.

STRC does not currently allow investors to exchange their shares for the underlying cryptocurrency. Adding such a feature could establish a clearer relationship between the preferred stock and Strategy’s assets, potentially creating a valuation floor. It would also expose the company to redemption demands that are absent from the current structure.

Meanwhile, Joe Burnett, the VP of Bitcoin Strategy at Strive, said that this lack of immediate redemption is an important distinction between Strategy and failed crypto systems such as TerraUSD.

Before TerraUSD collapsed in 2022, about $18.7 billion of the stablecoin was circulating against roughly $3.1 billion of Bitcoin reserves, while its design allowed holders to seek redemptions. Strategy, by comparison, holds more than $50 billion of Bitcoin against about $10.5 billion of STRC, and preferred shareholders cannot demand repayment in the underlying asset.

The comparison suggests Strategy is less vulnerable to the type of rapid run that overwhelmed Terra. Its risk is more gradual: a prolonged Bitcoin decline could raise financing costs, weaken demand for its securities, and force the company to dedicate more capital to dividends and interest payments.

However, Capriole Investments founder Charles Edwards sees a more fundamental problem. He argued that Strategy remains too reliant on Bitcoin appreciation and continued access to capital markets to support its obligations.

Edwards said the company should reduce debt and preferred-stock liabilities while developing sources of income that do not depend entirely on rising Bitcoin prices.

His proposals included collateralized lending and settlement services, as well as acquisitions of digital-asset treasury companies trading at steep discounts to the value of their holdings.

That approach would move Strategy closer to a Bitcoin-focused financial institution and away from a model centered primarily on raising capital to buy more of the cryptocurrency. It would also require the company to retreat from some of the securities it created to expand its treasury.

Despite these views, Strategy still has room to manage the downturn. Its Bitcoin holdings exceed $50 billion at current prices, and it has built a $1.4 billion reserve. Additionally, STRC investors cannot immediately redeem their shares against the treasury.

Those safeguards reduce the risk of a sudden liquidity event, but they do not resolve the rising cost of maintaining the structure.

A Bitcoin recovery would improve the value of Strategy’s holdings and could revive demand for both MSTR and STRC. A prolonged downturn would leave the company with less attractive options: increase the STRC dividend to support the preferred shares, issue common stock at weaker prices, reduce Bitcoin purchases or sell more of the treasury to meet cash obligations.

The debate is therefore less about whether Strategy can survive an underwater position in the near term than about how much it must spend to preserve its financing model until Bitcoin recovers.